Products You May Like

Dollar drops broadly today, partly due to month-end flows, and partly as position adjustment ahead of the first one-on-one Presidential debate between Donald Trump and Joe Biden. Nevertheless, Yen and Canadian Dollar are slightly weaker. On the other hand, Aussie and Kiwi are picking up some steam for a strong rebound. Trading in the stock markets are actually subdued. Resurgence in coronavirus infections in Europe saw daily cases in the Netherlands hit record high. Total deaths also passed the “agonizing milestone” of one million. But traders’ immune systems have already geared up against… pandemic news.

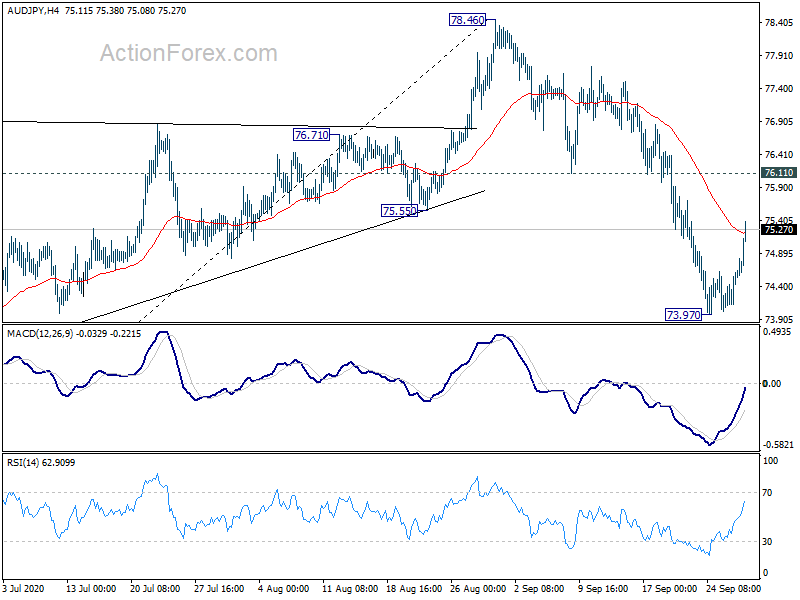

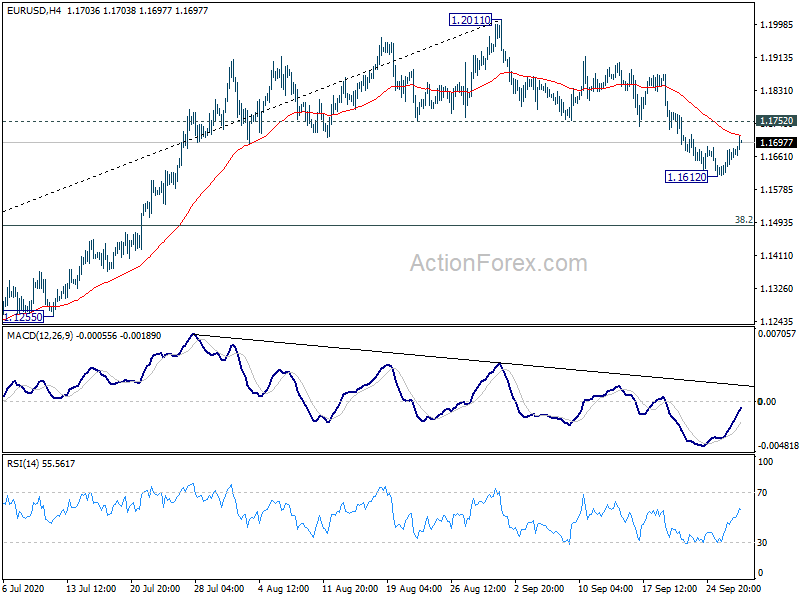

Technically, a couple of levels need to be taken out decisively to confirm that Dollar’s rebound has completed. The levels include 1.1752 resistance in EUR/USD, 1.3007 resistance in GBP/USD, 0.9200 support in USD/CHF. Meanwhile, AUD/USD and AUD/JPY will also have to overcome 0.7192 resistance and 76.11 resistance respectively to confirm completion of the corrective pull back. We’ll see how it goes.

– advertisement –

In Europe, currently, FTSE is down -0.36%. DAX is down -0.25%. CAC is down -0.01%. Germany 10-year yield is down -0.006 at -0.531. Earlier in Asia, Nikkei rose 0.12%. Hong Kong HSI dropped -0.85%. China Shanghai SSE rose 0.21%. Singapore Strait Times dropped -0.46%. Japan 10-year JGB yield dropped -0.0054 to 0.020.

US goods trade deficit widened to USD -82.9B in Aug

US goods trade deficit widened to USD -82.9B in August, from July’s USD -80.1B. larger than expectation of USD -81.8B. Exports of goods rose USD 3.2B over July to USD 118.3B. Imports of goods rose USD 6.0B to USD 201.3B. Wholesale inventories rose 0.5% mom to USD 637.0B. Retail inventories rose 0.8% mom to USD 599.7B.

Eurozone economic sentiment rose to 91.1, improvements in all large economies

Eurozone Economic Sentiment Indicator rose to 91.1 in September, up from 87.5, beat expectation of 89.4. EU ESI rose 3.4 pts to 90.2. The reading in both regions has so far recovered nearly 70% of the combined losses of March and April already. Employment Expectations Indicator also improved, up 2.3% to 91.8 in Eurozone, and up 2.4% to 91.8 in EU.

Looking at some details for the Eurozone, industrial confidence rose from -12.8 to -11.1. Services confidence rose form -17.2 to -11.1 Consumer confidence rose from -14.7 to -13.9. Retail trade confidence rose from -10.5 to -8.7. Construction confidence rose from -11.8 to -9.6.

From a country perspective, the ESI continued to recover in all the largest euro-area economies, namely in Italy (+8.4), France (+5.8), the Netherlands (+2.1), Spain (+1.6) and Germany (+1.2). All in all, in these countries, between 55 (Spain) and 80% (Germany) of confidence losses suffered during the lockdown were recovered.

Also released, Germany CPI came in at -0.2% mom, -0.2% yoy in September. From UK, mortgage approvals rose to 85k in August, up from 66k. M4 money supply dropped -0.4% mom in August, below expectation of 1.3% mom.

BoJ: Unlikely for Japan’s economy to rebound significantly

In the Summary of Opinions at BoJ’s September 16-17 meeting, it’s noted that it’s “unlikely” for Japan’s economy to “rebound significantly”. Domestic demand, mainly in services consumption, will “likely remain at a low level” due to the pandemic. A “clear V-shaped recovery” has been seen in some sectors, but recovery in demand is “still no in sight in other sectors”.

Year-on-year CPI is “likely to be negative for the time being”, is expected to “turn positive and then increase gradually with the economy improving”. Thus far, “deflationary price-setting behavior” for retaining customers “does not seem to have been widely observed”.

As of monetary policy, it’s necessary to focus on supporting corporate financing and sustaining employment. “If the economic recovery is delayed, the potential growth rate of Japan’s economy could decline through rises in bankruptcies of firms and unemployment, and the functioning of financial intermediation also could deteriorate, reflecting the materialization of credit risk.”

Also from Japan, Tokyo CPI core ticked up to -0.2% yoy in September, from August’s -0.3% yoy better than expectations.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1627; (P) 1.1654; (R1) 1.1692; More…..

EUR/USD’s recovery from 1.1612 extends higher today but stays below 1.1752 support turned resistance. Intraday bias remains neutral and further decline is still expected. On the downside, break of 1.1612 will extend the fall from 1.2011 short term top to 38.2% retracement of 1.0635 to 1.2011 at 1.1485. However, firm break of 1.1752 will suggest that the corrective pull back has completed. Intraday bias will be turned back to the upside for retesting 1.2011.

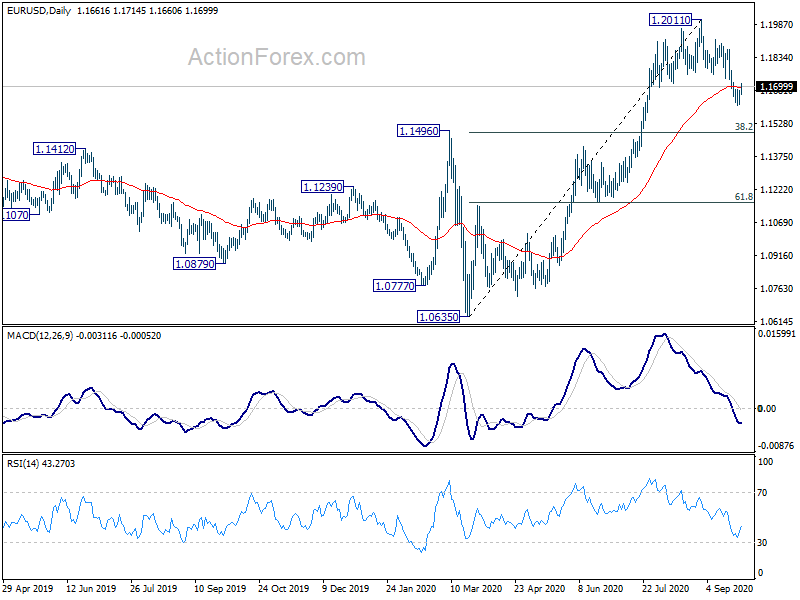

In the bigger picture, rise from 1.0635 is seen as the third leg of the pattern from 1.0339 (2017 low). Further rally rise should be seen to cluster resistance at 1.2555 next, (38.2% retracement of 1.6039 to 1.0339 at 1.2516 ). This will remain the favored case as long as 1.1422 resistance turned support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Core Y/Y Sep | -0.20% | -0.30% | -0.30% | |

| 08:30 | GBP | Mortgage Approvals Aug | 85K | 72K | 66K | |

| 08:30 | GBP | M4 Money Supply M/M Aug | -0.40% | 1.30% | 0.90% | |

| 09:00 | EUR | Eurozone Economic Sentiment Sep | 91.1 | 89.4 | 87.7 | 87.5 |

| 09:00 | EUR | Eurozone Services Sentiment Sep | -11.1 | -24.4 | -17.2 | |

| 09:00 | EUR | Eurozone Industrial Confidence Sep | -11.1 | -9.5 | -12.7 | -12.8 |

| 09:00 | EUR | Eurozone Consumer Confidence Sep F | -13.9 | -13.9 | -13.9 | -14.7 |

| 09:00 | EUR | Eurozone Business Climate Sep | -1.19 | -1.38 | -1.33 | -1.34 |

| 12:00 | EUR | Germany CPI M/M Sep P | -0.20% | -0.10% | -0.10% | |

| 12:00 | EUR | Germany CPI Y/Y Sep P | -0.20% | -0.10% | 0.00% | |

| 12:30 | USD | Goods Trade Balance (USD) Aug | -82.9B | -81.8B | -79.3B | -80.1B |

| 12:30 | USD | Wholesale Inventories Aug P | 0.50% | -0.20% | -0.30% | |

| 13:00 | USD | S&P/CS Composite-20 HPI Y/Y Jul | 3.60% | 3.50% | ||

| 14:00 | USD | Consumer Confidence Sep | 90 | 84.8 |