Products You May Like

Dollar’s post-FOMC strength continues to overwhelm the markets today. Though, Yen is also catching up as US futures point to a weak open. Selling in commodity Yen crosses is also helping the Japanese currency. Swiss Franc is currently the worst performing, as SNB sounded it’s fully in inertia despite better growth and inflation outlook. Kiwi and Aussie are the worst performing, but Euro and Sterling are not too far away.

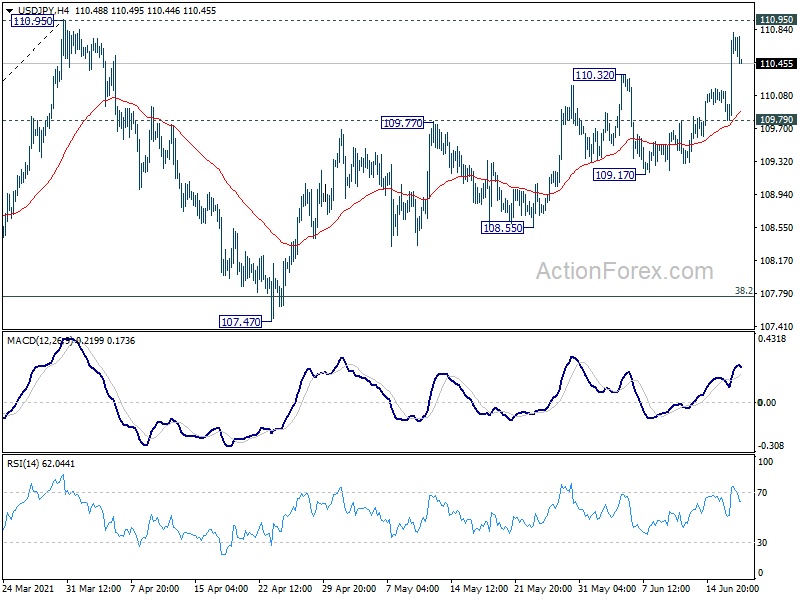

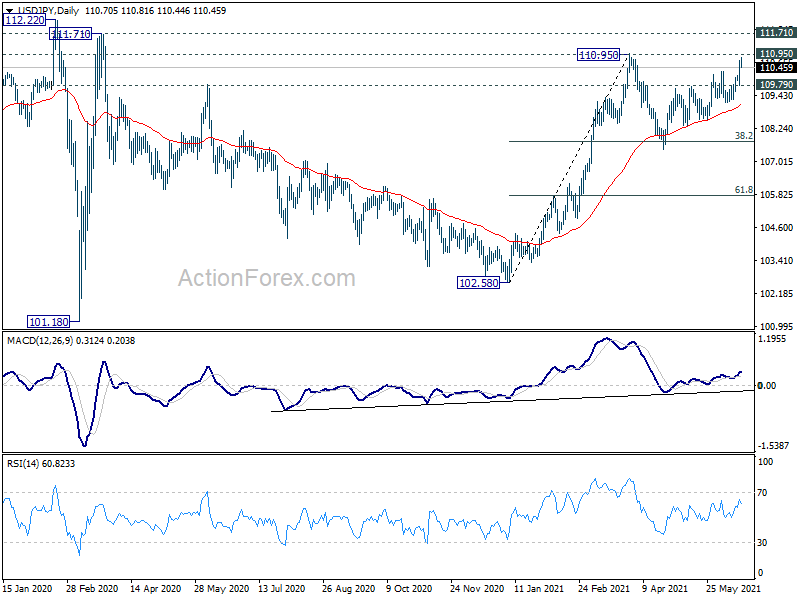

Technically, Dollar strength should be cleared with EUR/USD’s firm break of 1.2 handle. The question now is, when the greenback would continue to lead the Yen. Or, Yen would eventually overtake as risk aversion intensifies. USD/JPY is now facing 110.95 resistance. Decisive break there will resume larger rise from 102.58 and solidify Dollar’s place as winner. Rejection by 110.95, followed by break of 109.79 support, however, would suggests that USD/JPY is extending the consolidation form 110.95 with another fall. That would be a signal of deeper selloff in Yen crosses on risk aversion.

In Europe, at the time of writing, FTSE is down -0.62%. DAX is down -0.05%. CAC is down -0.13%. Germany 10-year yield is up 0.0203 at -0.227. Earlier in Asia, Nikkei dropped -0.93%. Hong Kong HSI rose 0.43%. China Shanghai SSE rose 0.21%. Singapore Strait Times dropped -0.04%. Japan 10-year JGB yield rose 0.016 to 0.066.

US initial jobless claims rose to 412k, continuing claims at 3.5m

US initial jobless claims rose 37k to 412k in the week ending June 12, above expectation of 360k. Four-week moving average of initial claims dropped -8k to 395k lowest since March 14, 2020. Continuing claims rose 1k to 3518k in the week ending June 5. Four-week moving average of continuing claims dropped -55k to 3608k, lowest since March 21, 2020.

Also released, Philly Fed manufacturing index dropped to 30.7 in June, down from 31.5, above expectation of 30.1.

SNB kept rate at -0.75%, upgrades GDP and inflation forecasts

SNB kept policy rate and interest on sight deposits at -0.75% as widely expected. It remains “willing to intervene in the foreign exchange market as necessary”. It reiterated that the Swiss franc is “highly valued”. The “expansionary monetary policy provides favourable financing conditions, contributes to an appropriate supply of credit and liquidity to the economy, and counters upward pressure on the Swiss franc.”

The new condition inflation forecasts are revised slightly higher to 0.4% in 2021 (from 0.2%), 0.6% in 2022 (from 0.4%) and 0.6% in 2023 (from 0.5%). 2021 GDP forecast was also revised up to 3.5%, “primarily attributable to the lower-than-expected decline in GDP and the first quarter”. GDP is “likely to return to its pre-crisis level by the middle of the year”.

Also from Swiss, trade surplus widened to CHF 4.95B in May, above expectation of CHF 4.23B.

Eurozone CPI finalized at 2.0% yoy in May, EU at 2.3% yoy

Eurozone CPI was finalized at 2.0% yoy in May, up from April’s 1.6% yoy. Highest contribution came from energy (+1.19 percentage points, pp), followed by services (+0.45 pp), non-energy industrial goods (+0.19 pp) and food, alcohol & tobacco (+0.15 pp).

EU CPI was finalized at 2.3% yoy, up from April’s 2.0% yoy. The lowest annual rates were registered in Greece (-1.2%), Malta (0.2%) and Portugal (0.5%). The highest annual rates were recorded in Hungary (5.3%), Poland (4.6%) and Luxembourg (4.0%). Compared with April, annual inflation fell in four Member States, remained stable in one and rose in twenty-two.

ECB Lane: From September there’s going to be a lot of things happening

ECB chief economist Philip Lane told Bloomberg TV that it’s “unnecessary and premature” to talk about tapering the asset purchase program.

“We know from September there’s going to be a lot of things happening,” he added. “It’s not a turn on a dime situation where we’re going to know everything at a point in time, but of course we’ll know a lot more over the summer.”

“Going back to September, we will have new forecasts, but remember we have a very strong forecast for quarter three, but quarter three is not over until the end of September,” he added. “We’re not necessarily going to have every piece of hard data you want to have going into the September meeting.”

Australia employment grew 115.2k in May, unemployment drop to pre-pandemic 5.1%

Australia employment rose 115.2k in May, above expectation of 30.0k. Full time jobs grew 97.5k. Part-time jobs rose 17.7k. Unemployment rate dropped to 5.1%, down from 5.5%, much better than expectation of of 5.5%. Participation rate also rose 0.3% to 66.2%.

Bjorn Jarvis, head of labour statistics at the ABS, said May was the seventh consecutive monthly fall in the unemployment rate. “The unemployment rate fell to 5.1 per cent, which was below March 2020 (5.3 per cent) and back to the level in February 2020 (5.1 per cent). The declining unemployment rate continues to align with the strong increases in job vacancies”.

New Zealand GDP grew 1.6% qoq in Q1, broad based growth

New Zealand GDP grew 1.6% qoq in Q1, much stronger than expectation of 0.5% qoq. Services industries rose 1.1% qoq. Goods producing industries rose 2.4% qoq. Primary industries rose 0.3% qoq. GDP per capita rose 1.5% qoq.

“After an easing of economic activity in the December quarter, we’ve seen broad-based growth in the first quarter of 2021. This is despite Auckland being in alert level 3 lockdown for 10 days, and continued border restrictions,” national accounts senior manager Paul Pascoe said.

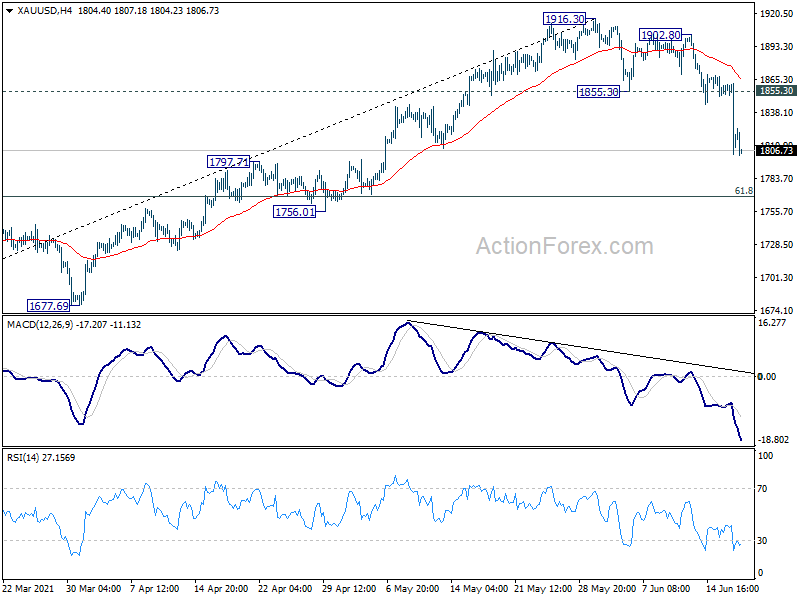

Gold pressing 1800 on downside acceleration, more decline ahead

Gold’s decline accelerates on broad based Dollar strength, and it’s now pressing 1800 handle. The strong break of 55 day EMA dampens our original bullish view. That is, rise from 1676.65 and fall from 1916.30 might both be legs of the consolidation pattern from 2075.18 only, which is still unfolding.

Deeper decline would now be seen to 61.8% retracement of 1676.65 to 1916.30 at 1768.19. Sustained break there will bring further fall to 1676.65 and below, to extend the pattern from 2075.18. Also, for now, risk will stay on the downside as long as 1855.30 support turned resistance holds, in case of recovery.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 109.98; (P) 110.08; (R1) 110.16; More…

Intraday bias in USD/JPY remains on the upside with focus on 110.95 high. Decisive break there will resume larger up trend from 102.58 to 111.71 key resistance next. However, break of 109.79 support will suggest rejection by 110.95. Intraday bias will be turned back to the downside for 109.17 support. Break there will extend the consolidation pattern from 110.95 with another falling leg, targeting 107.47 support again.

In the bigger picture, medium term outlook is staying neutral with 111.71 resistance intact. Though, as notable support was seen from 55 day EMA, rise from 102.58 is mildly in favor to extend higher. Decisive break of 111.71/112.22 resistance will suggest medium term bullish reversal. Rise from 101.18 could then target 118.65 resistance (Dec 2016) and above. However, sustained break of 55 day EMA would revive some medium term bearishness, and open up deep fall to 61.8% retracement of 102.58 to 110.95 at 105.77 and below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | GDP Q/Q Q1 | 1.60% | 0.50% | -1.00% | |

| 01:30 | AUD | Employment Change May | 115.2K | 30.0K | -30.6K | -30.7K |

| 01:30 | AUD | Unemployment Rate May | 5.10% | 5.50% | 5.50% | |

| 06:00 | CHF | Trade Balance (CHF) May | 4.95B | 4.23B | 3.84B | |

| 07:30 | CHF | SNB Interest Rate Decision | -0.75% | -0.75% | -0.75% | |

| 08:00 | CHF | SNB Press Conference | ||||

| 09:00 | EUR | Eurozone CPI Y/Y May F | 2.00% | 1.60% | 2.00% | |

| 09:00 | EUR | Eurozone CPI Core Y/Y May F | 1.00% | 0.90% | 0.90% | |

| 12:30 | USD | Initial Jobless Claims (Jun 11) | 412K | 360K | 376K | 375K |

| 12:30 | CAD | ADP Employment Change May | 351.3K | |||

| 12:30 | CAD | Foreign Securities Purchases (CAD) Apr | 9.95B | 4.35B | 4.12B | |

| 12:30 | USD | Philadelphia Fed Manufacturing Survey Jun | 30.7 | 30.1 | 31.5 | |

| 14:30 | USD | Natural Gas Storage | 71B | 98B |