Products You May Like

The BOE voted unanimously to keep Bank rate at 0.1%, and 7-1 to leave purchases of government bond at 875B pound. While the latter decision came less hawkish than we had anticipated (we expected 2 dissents), British pound got a boost as policymakers hinted about “modest tightening”.

Upgrading Inflation Forecast

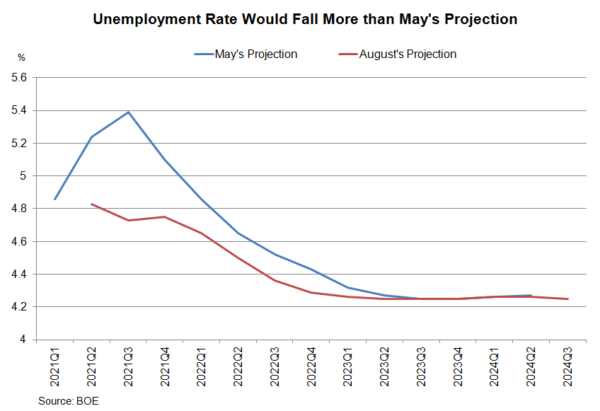

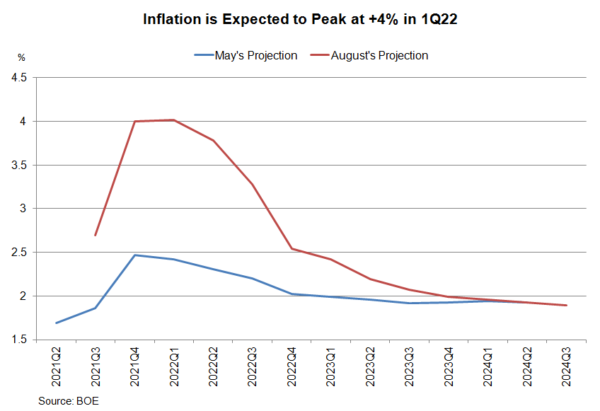

The staff revised higher 2Q21 GDP growth forecast to +5%, from +4.25% projected in May. Growth for 3Q21 was downgraded by -1 ppt to +2.9%. The economy is estimated to expand by +7.25% in 2021, unchanged from previously. In light of a resilient ob market, the staff projected that the unemployment rate would peak at 4.8%in 4Q21, compared with 5.4% in 3Q21 in May’s forecast. The unemployment rate would likely return to BOE’s natural rate in 4Q22, a quarter earlier than May’s forecast. The central bank estimated that inflation would peak at around +4% in 1Q22, compared with previous projection of +2.5% in 4Q21. The upgrade was driven by the recent stronger-than-expected CPI data, and re-opening effects in services and input cost pass-through in consumer goods.

The central bank estimated that inflation would peak at around +4% in 1Q22, compared with previous projection of +2.5% in 4Q21. The upgrade was driven by the recent stronger-than-expected CPI data, and re-opening effects in services and input cost pass-through in consumer goods.

Policymakers acknowledged that the continued increase in price pressures reflected “the speed and unevenness of the recovery in activity, and disruptions to supply chains”. Yet, they reiterated that such pressures would be transitory. As noted in the statement, “current elevated global and domestic cost pressures will prove transitory. Nonetheless, the economy is projected to experience a more pronounced period of above-target inflation in the near term than expected in the May Report. And, alongside temporary constraints on supply, the rapid recovery in demand has eroded spare capacity such that the economy is projected to have a margin of excess demand for a period”. The committee remained divided over whether the +2% inflation target has been met. Some members suggested that “although considerable progress has been made in achieving the conditions of that guidance, the conditions are not yet met fully, while others judged that “the conditions of the guidance have been met fully, but note that the guidance made clear that these have only ever been necessary not sufficient conditions for any future tightening in monetary policy”.

Modest Tightening Approaching

While all the monetary policy measures stay unchanged, the central bank indicated that “modest tightening” could be necessary if the economy continues to improve. As noted in the statement, “should the economy evolve broadly in line with the central projections in the August Monetary Policy Report, some modest tightening of monetary policy over the forecast period is likely to be necessary to be consistent with meeting the inflation target sustainably in the medium term”.

In its updated monetary policy exit guidance, the BOE would begin reducing its balance sheet when the Bank rate hits 0.5% (currently at 0.1%), compared with previous guidance of 1.5%. It would also consider actively selling assets once the policy rate reaches 1%. The subtle changes signal that the unwinding of the balance sheet could come more quickly than previously anticipated.