Products You May Like

New Zealand Dollar trades mildly lower together with commodity currencies in quiet Asian session. Overall markets are mixed as Japan and Hong Kong stocks head lower, decoupling from the strong rebound in the US overnight. Dollar appears to be supported by the rise in treasury yields, with 10-year yield back above 1.5 handle. Yen is also turning softer on the development. But the moves are so far indecisive. Focus will now turn to ADP employment from the US for some inspirations.

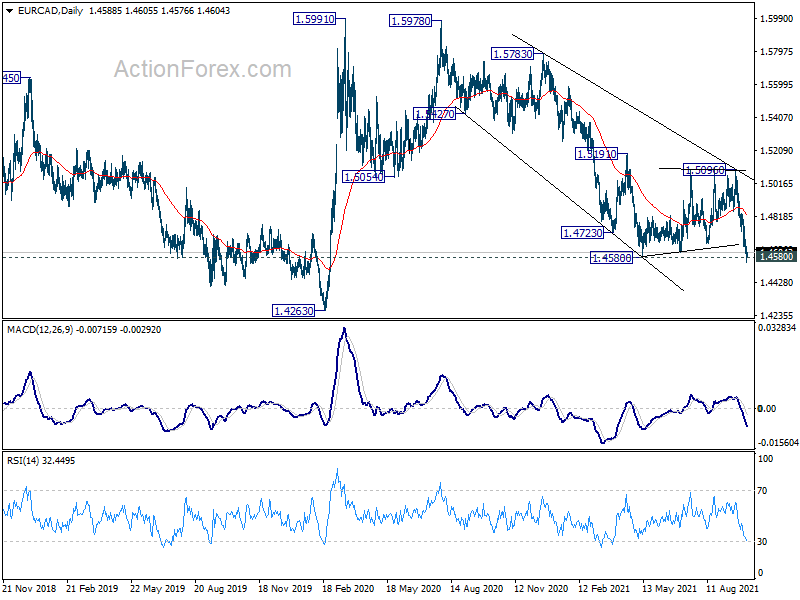

Technically, EUR/CAD’s breached 1.4580 support argues that it’s resuming the down trend from 1.5978. Focus will firstly be on whether it could sustain below the support level and set the stage for deeper fall towards 1.4263. Secondly, we’d also keep an eye on whether USD/CAD would accelerate down through 1.2492 support (which is not happening yet). Or EUR/USD would break through 1.1561 temporary low to resume larger fall from 1.2265.

In Asia, at the time of writing, Nikkei is down -1.0)%. Hong Kong HSI is down -0.71%. Singapore Strait Times is up 0.11%. Japan 10-year JGB yield is up 0.0265 at 0.084. China is still on holiday. Overnight, DOW rose 0.92%. S&P 500 rose 1.05%. NASDAQ rose 1.25%. 10-year yield rose 0.048 to 1.529.

RBNZ hikes OCR to 0.50%, maintains hawkish bias

RBNZ raised the Official Cash Rate by 25bps to 0.50% as widely expected, as “it is appropriate to continue reducing the level of monetary stimulus so as to maintain low inflation and support maximum sustainable employment.” It maintains a hawkish bias and said, “further removal of monetary policy stimulus is expected over time, with future moves contingent on the medium-term outlook for inflation and employment.”

In the accompany statement, it’s noted that current COVID-19-related restrictions “have not materially changed the medium-term outlook” for inflation and employment. Capacity pressures “remain evident” and economic data highlighted that the economy “has been performing strongly in aggregate”. Headline CPI is expected to rise above 4% in the near term before returning towards 2% target midpoint over the medium term.

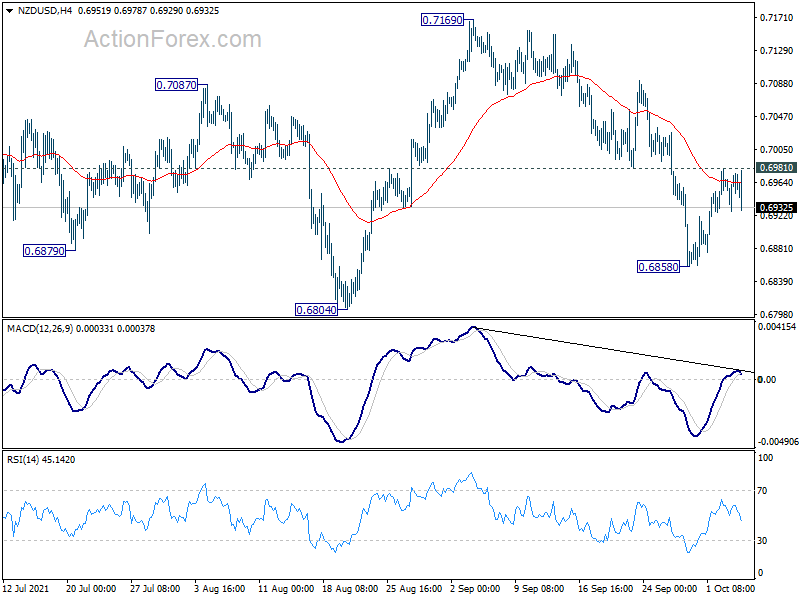

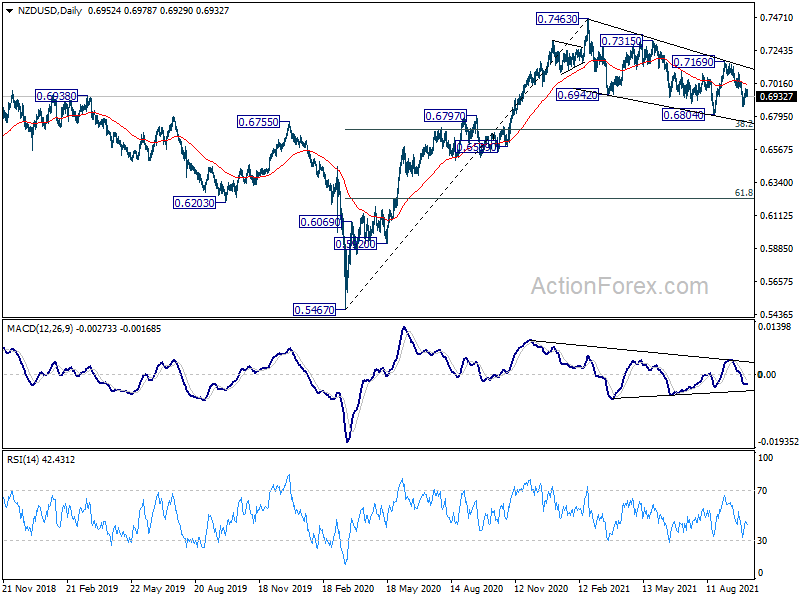

NZD/USD dips mildly after RBNZ hike

NZD/USD dips mildly after RBNZ rate hike but is bounded in very tight range. Rebound from 0.6858 is limited by 0.6981 minor resistance so far. Hence, fall from 0.7169 is still mildly in favor to extend lower. Break of 0.6858 will target 0.6804 low first.

Also, NZD/USD is still staying in the corrective pattern from 0.7463 high. Break of 0.6804 will target 38.2% retracement of 0.5467 to 0.7463 at 0.6701. This will remain the favored case as long as 0.7169 resistance holds, even in case of stronger rebound.

BoJ Kuroda: No pressing need for firms to raise wages and selling prices

BoJ Governor Haruhiko Kuroda said in a speech, Japan’s economy has “picked up”, led by exports and the manufacturing sector. “If Japan can simultaneously protect public health and improve consumption activities through the use of vaccination certificates, for example, the economic recovery trend is very likely to become more pronounced, even in the services sector, also supported by the materialization of pent-up demand,” he added.

On the contrasting development in CPI compared with the US, Kuroda said demand in Japan “has not recovered as rapidly as that in the U.S”. Also, “many Japanese firms have essentially maintained their labor, supply-side constraints in Japan have not been as severe as in the U.S., and there has been no pressing need for firms to raise wages and selling prices.”

Looking ahead

Germany factory orders, UK construction PMI and Eurozone retail sales will be released in European session. US will release ADP employment later in the day.

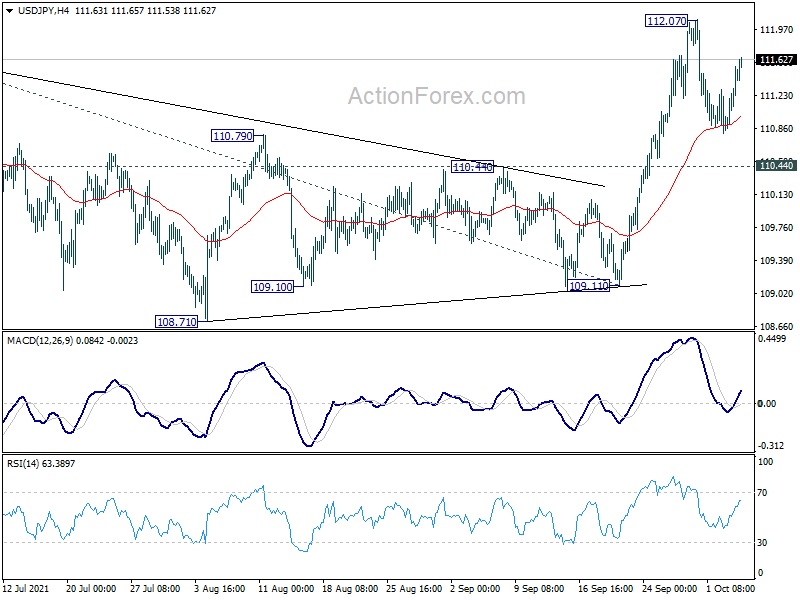

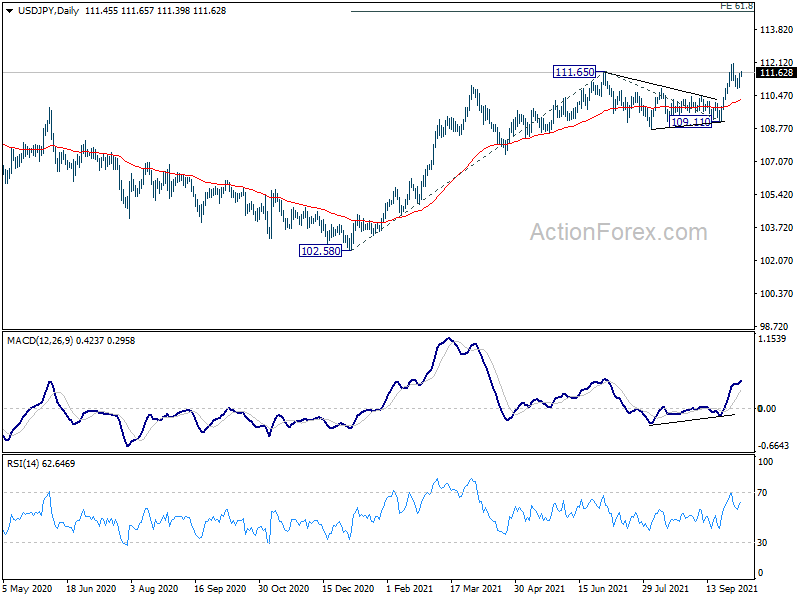

USD/JPY Daily Outlook

Daily Pivots: (S1) 111.04; (P) 111.30; (R1) 111.73; More…

USD/JPY rebounds after drawing support from 4 hour 55 EMA, but stays below 112.07 resistance. Intraday bias remains neutral first. Another retreat cannot be ruled out, but downside should be contained by 110.44 support to bring another rally. On the upside, above 112.07 will extend larger rise to 61.8% projection of 102.58 to 111.65 from 109.11 at 114.71 next. However, break of 110.44 will dampen the bullish case and turn focus back to 109.11 support.

In the bigger picture, break of 111.71 resistance suggests that the whole corrective decline from 118.65 (2016 high) has completed at 101.18 (2020 low) already. Medium term bullishness is also affirmed as USD/JPY stays well above 55 week EMA (now at 108.60). Sustained trading above 111.71 will affirm this bullish case. Rise from 101.18 could then be resuming whole rally from 98.97 (2016 low) through 118.65. This will now be the preferred case as long as 108.71 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:00 | NZD | RBNZ Rate Decision | 0.50% | 0.50% | 0.25% | |

| 01:00 | NZD | RBNZ Rate Statement | ||||

| 06:00 | EUR | Germany Factory Orders M/M Aug | -1.50% | 3.40% | ||

| 08:30 | GBP | Construction PMI Sep | 53.9 | 55.2 | ||

| 09:00 | EUR | Eurozone Retail Sales M/M Aug | 0.80% | -2.30% | ||

| 12:15 | USD | ADP Employment Change Sep | 475K | 374K | ||

| 14:30 | USD | Crude Oil Inventories | 0.8M | 4.6M |