Products You May Like

Worries about Omicron remains a main theme in the markets. Nikkei takes a dive after Japan announced to close its borders to all foreigners as Prime Minister Fumio Kishida said he’s taking measures with a “strong sense of crisis”. The forex markets are relatively quiet for now, with Yen and Swiss Franc digesting some of last week’s gains. Commodity currencies are also recovering slightly. But overall, the range in currency pairs is tight.

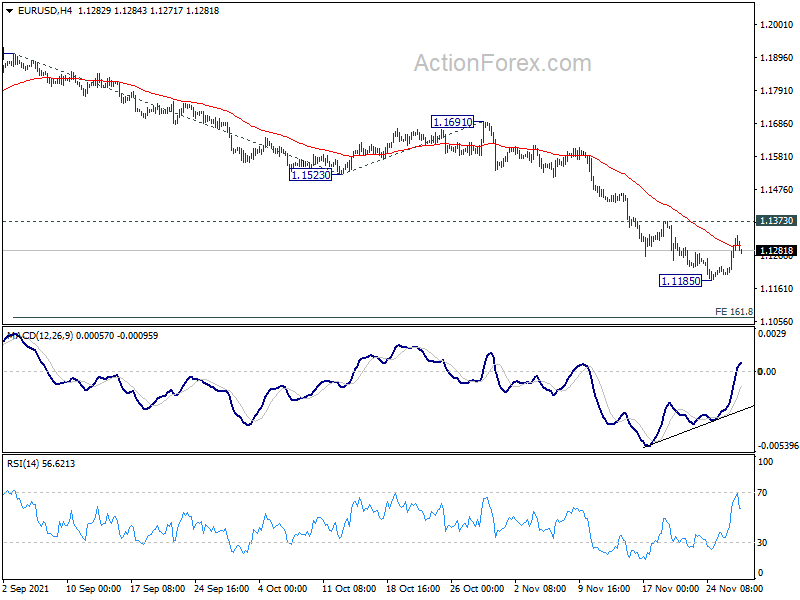

Technically, the rallies in Swiss Franc and Yen are just taking a breather and we’d expect them to resume sooner or later. The question for the week is whether risk-off sentiment would boost Dollar or Euro more. EUR/USD’s weak recovery from 1.1185 doesn’t warrant a stronger rebound yet. But break of 1.1373 minor resistance will indicate that the tide has turned for the near term.

In Asia, at the time of writing, Nikkei is down -1.78%. Hong Kong HSI is down -1.22%. China Shanghai SSE is down -0.52%. Singapore Strait Times is down -1.17%. Japan 10-year JGB yield is down -0.0074 at 0.070.

ECB Lagarde: We are all better equipped to respond to Omicron

ECB President Christine Lagarde said over the weekend that there is an “obvious concern” about the Eurozone economic recovery with the new Omicron variant. But she added, “I believe we have learnt a lot”.

“We now know our enemy and what measures to take. We are all better equipped to respond to a risk of a fifth wave or the Omicron variant”, she said to Italian broadcaster RAI.

“The crisis taught us this virus knows no boundaries. Therefore we will not be protected until we are all vaccinated”, Lagarde said.

ECB Panetta: Intervening on inflation now creates more damage than benefit

ECB Executive Board member Fabio Panetta said the current inflation in Eurozone is bad but also temporary. It’s driven by supply chain disruptions and energy prices which are “bound to be overcome”. He would be among the first in favor to intervene if inflation are becoming more permanent.

But he added, “the central bank is not intervening because if it did, it would create more damage than benefit. It’s like an illness, not all medicines are good for all illnesses.”

RBNZ Ha: Omicron doesn’t change economic outlook, just reinforces downside risks

In a WSJ interview, RBNZ chief economic Yuong Ha said the central bank would have raised interest rate even if Omicron was know before the meeting last week.

He said New Zealand is now “transitioning into a new Covid protection framework” and people are “getting used to the idea of living with Covid”. Hence, Omicron doesn’t change the outlook. “It probably just reinforces the downside risks we saw in the projections,” he said.

RBNZ will be in a better place to assess Omicron’s economic impact at next meeting in February. “If Omicron turns out to be a massive game changer, that might be kind of like August where we just took a pause,” Ha said.

A busy week full of key data

A number of important economic data will be released this week. US consumer confidence, ISM indexes and non-farm payroll will catch most attention. Eurozone will release CPI flash, PPI, unemployment rate, retail sales. Focuses will also be on Canada employment, Australia GDP, and China PMIs.

But, the economic would be overshadowed by news regarding Omicron variant and the impact on risk sentiment.

Here are some highlights for the week:

- Monday: Japan retail sales; Germany CPI flash; UK mortgage approvals, M4 money supply; Canada current account, IPPI and RMPI; US pending home sales.

- Tuesday: Japan unemployment rate, industrial production, housing starts; Australia building approvals, current account; China official PMIs; France GDP; Swiss KOF economic barometer; Germany unemployment; Eurozone CPI flash; Canada GDP; US house price index, Chicago PMI, consumer confidence.

- Wednesday: Australia AiG manufacturing, GDP; New Zealand building permits; Japan capital spending, PMI manufacturing final; China Caixin PMI manufacturing; Germany retail sales; Swiss CPI, PMI manufacturing; Eurozone PMI manufacturing final; UK PMI manufacturing final; US ADP employment, ISM manufacturing, construction spending, Fed’s Beige Book; Canada PMI manufacturing.

- Thursday: Australia retail sales, trade balance, Japan consumer confidence; Swiss retail sales; Eurozone PPI, unemployment rate; US Challenger job cuts, jobless claims.

- Friday: Australia AiG construction; China Caixin PMI services; France industrial production; Eurozone PMI services, retail sales; UK PMI services’ Canada employment; US non-farm payrolls, ISM services, factory orders.

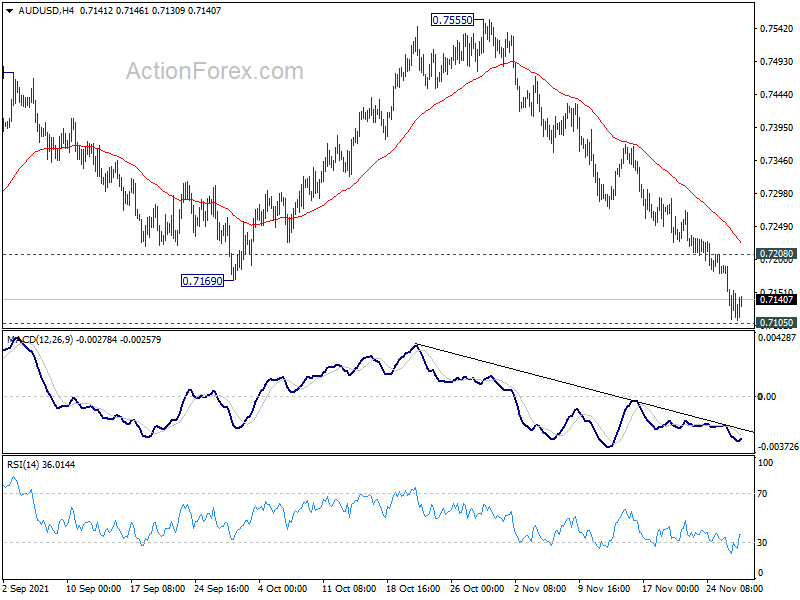

AUD/USD Daily Report

Daily Pivots: (S1) 0.7092; (P) 0.7143; (R1) 0.7174; More…

Intraday bias in AUD/USD remains on the downside for the moment. Break of 0.7105 support will confirm resumption of whole decline form 0.8006. Next target should be 0.6991 key structural support. On the upside, break of 0.7208 minor resistance will delay the bearish case and turn intraday bias neutral first.

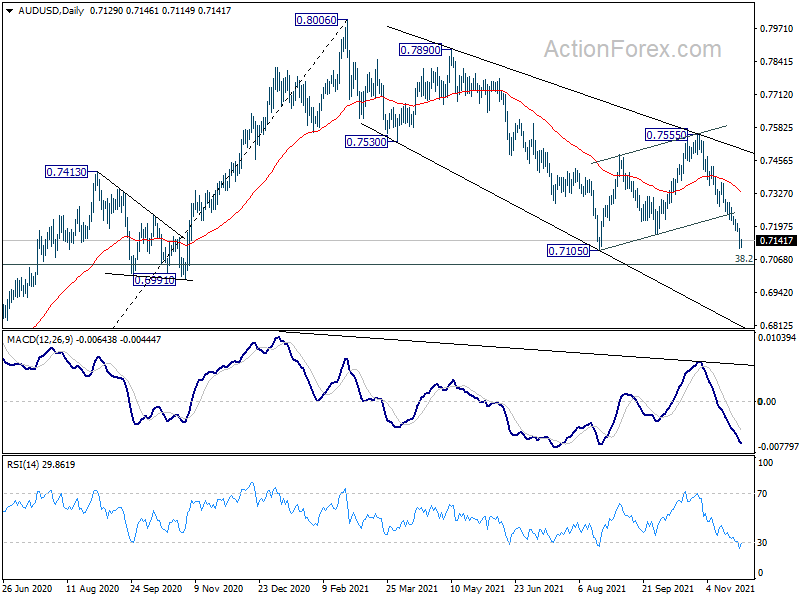

In the bigger picture, with 0.6991 cluster support (38.2% retracement of 0.5506 to 0.8006 at 0.7051) intact, we’re seeing price action from 0.8006 as a correction only. That is, up trend from 0.5506 low would resume after the correction completes. However, sustained break of 0.6991 will argue that the whole medium term trend has probably reversed. Deeper fall would be seen to 61.8% retracement at 0.6461.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Retail Trade Y/Y Sep | 0.90% | 1.10% | -0.50% | |

| 0:30 | AUD | Company Gross Operating Profits Q/Q Q3 | 4.00% | 3.00% | 7.10% | |

| 9:30 | GBP | Mortgage Approvals Oct | 71.250K | 72.645K | ||

| 9:30 | GBP | M4 Money Supply M/M Oct | 0.50% | 0.60% | ||

| 10:00 | EUR | Eurozone Economic Sentiment Indicator Nov | 117.5 | 118.6 | ||

| 10:00 | EUR | Eurozone Industrial Confidence Nov | 13.9 | 14.2 | ||

| 10:00 | EUR | Eurozone Services Sentiment Nov | 16.3 | 18.2 | ||

| 10:00 | EUR | Eurozone Consumer Confidence Nov F | -6.8 | -6.8 | ||

| 13:00 | EUR | Germany CPI M/M Nov P | -0.50% | 0.50% | ||

| 13:00 | EUR | Germany CPI Y/Y Nov P | 5.00% | 4.50% | ||

| 13:30 | CAD | Industrial Product Price M/M Oct | 1.00% | |||

| 13:30 | CAD | Raw Material Price Index Oct | 2.50% | |||

| 13:30 | CAD | Current Account (CAD) Q3 | 4.4B | 3.6B | ||

| 15:00 | USD | Pending Home Sales M/M Oct | 1.00% | -2.30% |