Products You May Like

Yen dropped broadly overnight as US stocks rebounded and stays soft in Asian session. Canadian Dollar also pare back some losses as WTI crude oil recovered back above 70 handle. But overall markets are generally mixed in holiday mood. Euro is currently the strongest for the week, followed by Kiwi and Sterling. Yen is the weakest followed by Canadian and Dollar.

Technically, we’ll keep an eye on the development in WTI crude oil today. It looks like retreat from 73.66 is finished at 66.46 already. Break of 73.66 will resume the rebound from 62.90 to 100% projection of 62.90 to 73.66 from 66.46 at 77.22. Such development, if happens, could help Loonie rebound further.

In Asia, at the time of writing, Nikkei rose is trading up 0.18%. Hong Kong HSI is up 0.33%. China Shanghai SSE is up 0.01%. Singapore Strait Times is up 0.08%. Overnight, DOW rose 1.60%. S&P 500 rose 1.78%. NASDSAQ rose 2.40%. 10-year yield rose 0.068 to 1.487.

BoJ minutes: members discussed impact of Yen’s depreciation

In the minutes of October 27-28 meeting, BoJ said “yen had depreciated somewhat significantly against both the U.S. dollar and the euro, mainly due to rises in U.S. and European interest rates”. Members have discussed the impact of the yen’s depreciation.

Some members said, “the depreciation had positively affected Japan’s economy as a whole through an increase in profits from business conducted overseas and a rise in stock prices, although its effect of pushing up exports had declined.”

One member said, “the effect of the depreciation on each economic entity was uneven, depending on industry and size”. Another member noted, “while prices had increased recently, triggered mainly by the yen’s depreciation, it was unlikely at present that heightened inflationary pressure would reduce the economic welfare of Japan as a whole.”

Australia Westpac leading index rose to -0.2%, Omicron not derailing recovery

The six month annualized growth rate in Westpac-Melbourne Institute Leading Index rose from -0.5% to -0.2% in November. The index has been in negative territory for three consecutive months, partly reflecting the lockdowns in New South Wales and Victoria. Nevertheless, reopening rebounds should eventually lift growth back above trend.

Westpac said both itself and the RBA “currently believe that Omicron will not derail the recovery although the next month will determine the extent of the delay and uncertainty.”

Looking ahead

UK will release Q3 GDP final and current account in European session. US will also release Q3 GDP final, existing home sales and consumer confidence.

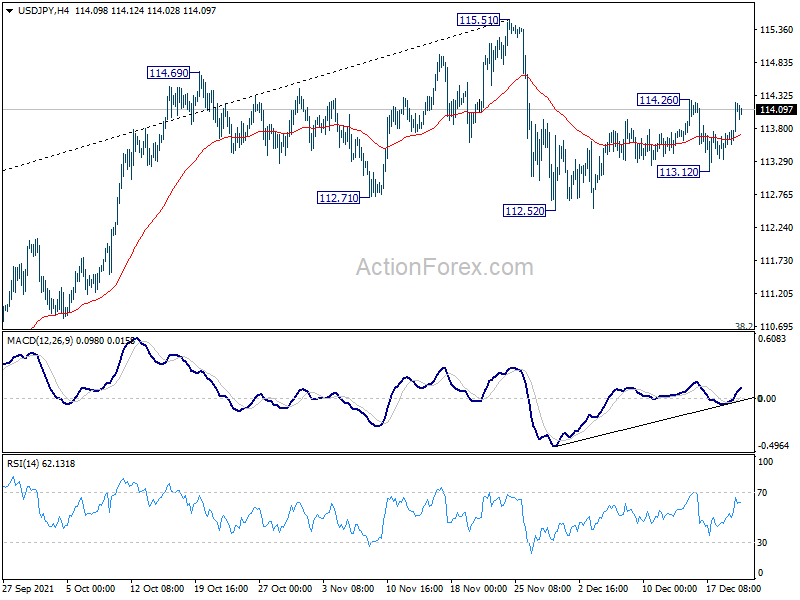

USD/JPY Daily Outlook

Daily Pivots: (S1) 113.69; (P) 113.96; (R1) 114.36; More…

Intraday bias in USD/JPY remains neutral first. On the upside, break of 114.26 resistance will resume the rebound from 112.52, towards 115.51 high. On the downside, break of 113.12 will turn bias to the downside, and resume the correction from 115.51 through 112.52 support.

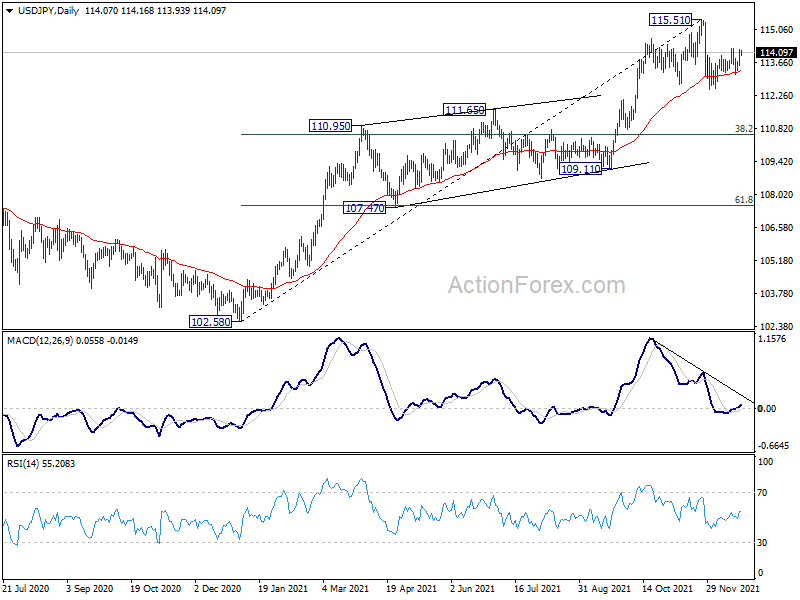

In the bigger picture, no change in the view that rise from 102.58 is the third leg of the up trend from 101.18 (2020 low). Such rally should target a test on 118.65 (2016 high) on resumption. However, firm break of 109.11 structural support will argue that the trend might have reversed and bring deeper fall to 107.47 support and possibly below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | AUD | Westpac Leading Index M/MNov | 0.10% | 0.20% | 0.30% | |

| 23:50 | JPY | BoJ Minutes | ||||

| 7:00 | GBP | GDP Q/Q Q3 F | 1.30% | 1.30% | ||

| 7:00 | GBP | Current Account (GBP) Q3 | -15.6B | -8.6B | ||

| 13:30 | USD | GDP Annualized Q3 F | 2.10% | 2.10% | ||

| 13:30 | USD | GDP Price Index Q3 F | 5.90% | 5.90% | ||

| 14:00 | CHF | SNB Quarterly Bulletin Q4 | ||||

| 15:00 | USD | Existing Home Sales M/M Nov | 6.5M | 6.34M | ||

| 15:00 | USD | Consumer Confidence Dec | 109.5 | |||

| 15:30 | USD | Crude Oil Inventories | -4.6M |