Products You May Like

Swiss Franc falls broadly today as other parts of the markets turned mixed. US treasury yield extends its sharp rally. But the impact on Dollar is some what offset by impressive rally in Germany and UK yields too. Euro recovers mildly but remains the worst performing one for the week, followed by Yen, and then Swiss. Australian Dollar is still the strongest one, followed by Kiwi and Loonie. But Dollar might pick up momentum again if supported by more hawkish comments from Fed policymakers.

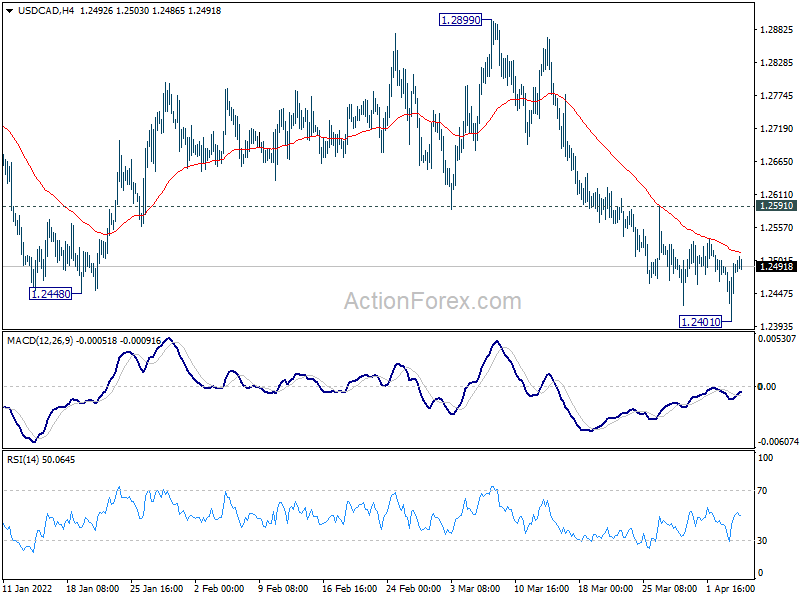

Technically, one focus for the end of the week is on whether Dollar could overpower commodity currencies. For now, as long as 0.7455 minor support in AUD/USD holds, further rise is expected through 0.7660 temporary top. As for USD/CAD, as long as 1.2591 minor resistance holds, deeper decline is expected through 1.2401. However, break of these two levels will argue that Dollar is striking back.

In Europe, at the time of writing, FTSE is down -0.28%. DAX is down -1.89%. CAC is down -1.93%. Germany 10-year yield is up 0.0464 at 0.665. Earlier in Asia, Nikkei dropped -1.58%. Hong Kong HSI dropped -1.87%. China Shanghai SSE rose 0.02%. Singapore Strait Times dropped -0.64%. Japan 10-year JGB yield rose 0.0338 to 0.245.

ECB Panetta: Holding inflation at 2% with high imported inflation could induce domestic deflation

ECB Executive Board member Fabio Panetta said in a speech that the high inflation in Eurozone is “mostly due to global factors – including the increase in the prices of oil, gas and other commodities – over which monetary policy has little leverage.” And it “does not fundamentally result from an economy that is running above potential”.

Therefore, “asking monetary policy alone to bring down short-term inflation while inflation expectations remain well anchored would be extremely costly”. Monetary tightening would not affected imported energy and food prices, but “massively suppress domestic demand to bring down inflation”.

“And with the current levels of imported inflation, in order to hold headline inflation to 2%, we would need domestic inflation to be deeply negative. In other words, we would induce domestic deflation,” he added.

Panetta suggested that “fiscal policy can help mitigate the challenge of higher inflation by containing the effects of higher energy prices”. On the other hand, “Monetary policy will play its role, adjusting policy in line with the medium-term inflation outlook. ”

ECB de Guindos: Green energy is a key priority for environment and security

ECB Vice President Luis de Guindos said in a speech, “for the euro area, the financial stability impact of the war has so far been relatively contained.” And, “markets have generally been functioning well”, with “no dash for cash”.

“While both banks and non-banks have been affected – especially the few that have large direct exposures to Russia and Ukraine – the economic fallout has not had a sizeable impact on the EU banking or financial systems as a whole,” he added.

But he also noted, “the invasion of Ukraine also demonstrated how vulnerable Europe is due to its high dependency on fossil fuel imports from Russia. Speeding up the green transition is a key priority from this perspective too – not only to address the urgent environmental and climate challenges we face, but also to help increase our energy security and protect the EU economy from energy price spikes.”

Eurozone PPI rose 1.1% mom, 31.4% yoy in Feb

Eurozone PPI rose 1.1% mom, 3.1.4% yoy in February, below expectation of 1.3% mom, 31.6% yoy. For the month, industrial producer prices increased by 1.6% for intermediate goods, by 1.3% in the energy sector, by 0.8% for non-durable consumer goods, by 0.6% for durable consumer goods and by 0.3% for capital goods. Prices in total industry excluding energy increased by 0.9%.

EU PPI rose 1.1% mom, 31.1% yoy. The highest monthly increases in industrial producer prices were recorded in Slovakia (+13.6%), Slovenia (+5.7%) and Greece (+4.8%). Decreases were observed in Ireland (-8.1%), Finland (-0.5%), Latvia (-0.3%), and Bulgaria (-0.1%).

UK PMI construction unchanged at 59.1, but optimism tumbled

UK PMI Construction was unchanged at 59.1 in March, better than expectation of 57.3. The latest reading signalled the join-fastest rate of output growth since June 2021. However, business optimism dropped to 17-month low.

Tim Moore, Economics Director at S&P Global: “Escalating fuel, energy and commodity prices led to the fastest rise in costs for six months. Intense inflationary pressures appear to have unnerved some construction companies. Business optimism slipped to its lowest since October 2020 on concerns that clients will cut back spending in response to rising prices and heightened economic uncertainty.”

China PMI composite dropped to 43.9, downward pressure aggravated by several factors

China Caixin PMI Services dropped sharply from 50.2 to 42.0 in March, much worse than expectation of 49.9. That’s also the worst reading since February 2020. PMI Composite dropped from 50.1 to 43.9, also the worst since February 2020.

Wang Zhe, Senior Economist at Caixin Insight Group said: “At present, China is facing the most severe wave of outbreaks since the beginning of 2020. Uncertainty also increased abroad. The outcome of the war between Russia and Ukraine is uncertain, and the commodity market has convulsed. Several factors have aggravated the downward pressure on China’s economy and underscore the risk of stagflation.”

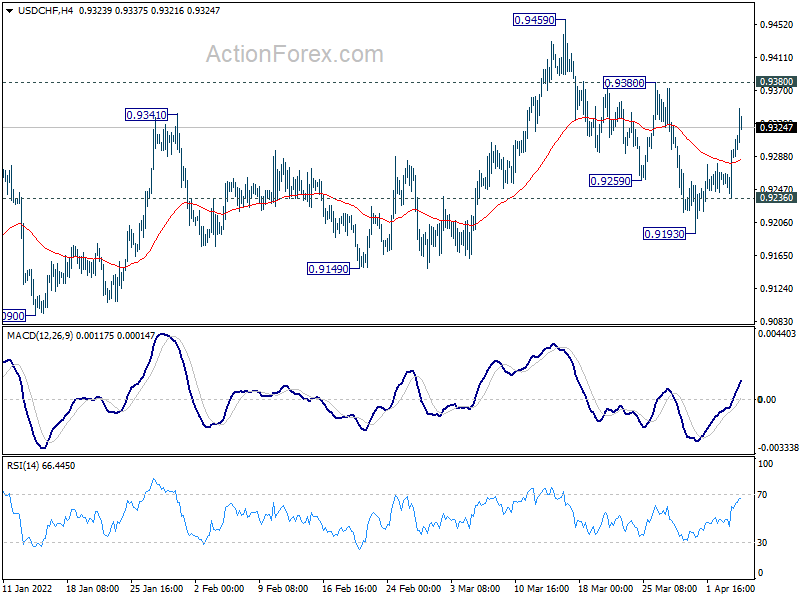

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9256; (P) 0.9277; (R1) 0.9316; More….

USD/CHF’s rebound from 0.9193 extends higher today but stays below 0.9380 resistance. Intraday bias remains neutral first. On the upside, break of 0.9380 will indicate that fall from 0.9459 has completed with three wave down to 0.9193. Such development will revive near term bullishness and turn bias back to the upside for 0.9459 and then 0.9471 resistance. On the downside, however, below 0.9236 will turn bias to the downside for 0.9149 structural support next.

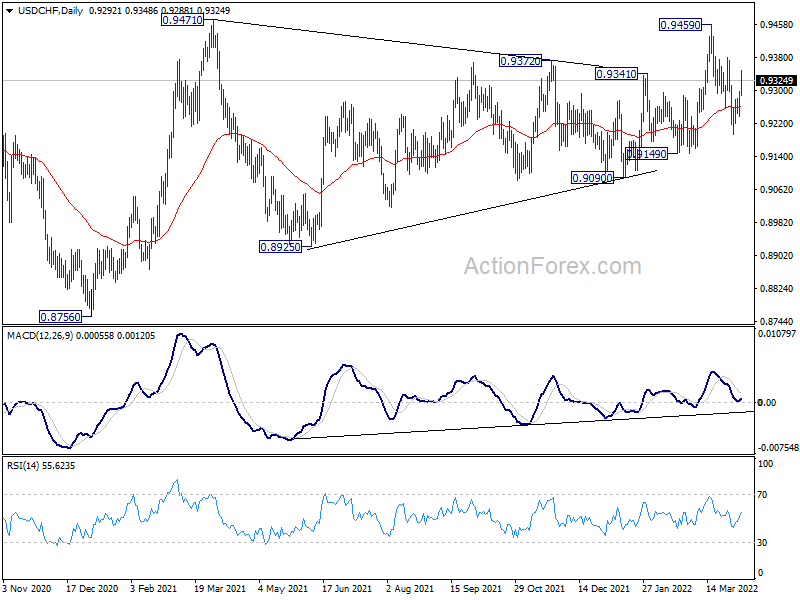

In the bigger picture, medium term outlook will be neutral at best as long as 0.9471 resistance holds. Larger down trend could still extend through 0.8756 (2021 low). However, firm break of 0.9471 will argue that whole down trend form 1.0342 (2016 high), has completed with waves down to 0.8756. A medium term up trend should be set up to target 1.0237/0342 resistance zone.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:45 | CNY | Caixin Services PMI Mar | 42 | 49.9 | 50.2 | |

| 06:00 | EUR | Germany Factory Orders M/M Feb | -2.20% | -0.20% | 1.80% | 2.30% |

| 08:30 | GBP | Construction PMI Mar | 59.1 | 57.3 | 59.1 | |

| 09:00 | EUR | Eurozone PPI M/M Feb | 1.10% | 1.30% | 5.20% | |

| 09:00 | EUR | Eurozone PPI Y/Y Feb | 31.40% | 31.60% | 30.60% | |

| 14:00 | CAD | Ivey PMI Mar | 62.3 | 60.6 | ||

| 14:30 | USD | Crude Oil Inventories | -2.9M | -3.4M | ||

| 18:00 | USD | FOMC Minutes |