Products You May Like

Lots of important economic data are released today but they’re largely ignored. Inflation data from the US and Eurozone are strong. Canada’s monthly GDP growth was well above expectation while Eurozone GDP growth turned weaker in Q1. But reactions to them are mild. While the greenback is paring some recent gains, it remains the strongest one for the week, followed by Canadian. Euro is still the worst performer, followed by Sterling and then Swiss Franc. Yen is mixed awaiting the next move.

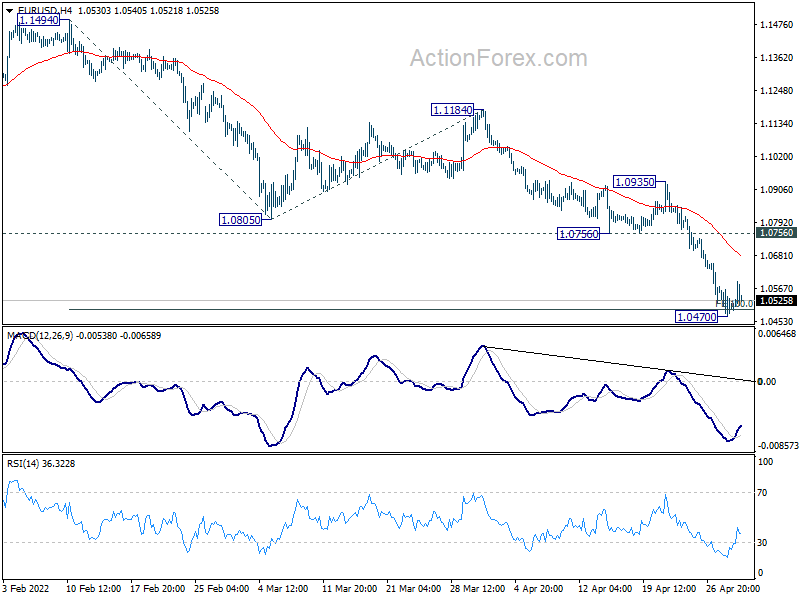

Technically, Dollar appears to be losing much upside momentum, but there is no sign of a turn around. EUR/USD would probably consolidate above 1.05 handle for a while. But outlook will stay bearish as long as 1.0756 resistance holds. Nevertheless, break of 1.2675 resistance turned support in USD/CAD, if happens, could be an early warning that Dollar is turning into a near term consolidation phase.

In Europe, at the time of writing, FTSE is up 0.60%. DAX is up 1.15%. CAC is up 0.90%. Germany 10-year yield is up 0.0206 at 0.924. Earlier in Asia, Nikkei rose 1.75%. Hong Kong HSI rose 4.01%. China Shanghai SSE rose 2.41%. Singapore Strait Times rose 0.65%. Japan 10-year JGB yield dropped -0.0310 to 0.219.

US PCE price index rose to 6.6% yoy, but core PCE ticked down to 5.2% yoy

US personal income rose 0.5% mom or USD 107.2B in March, slightly above expectation of 0.4% mom. Spending rose 1.1% mom or USD 185.0B, above expectation of 0.6% mom.

Headline PCE price index accelerated from 6.3% yoy to 6.6% yoy, above expectation of 6.5% yoy. Excluding good and energy, PCE core price index ticked down from 5.3% yoy to 5.2% yoy, below expectation of 5.3% yoy. Energy prices increased 33.9% yoy while food prices rose 9.2% yoy.

Canada GDP grew 1.1% mom in Feb, to grow further in Mar

Canada GDP grew strongly by 1.1% mom in February, above expectation of 0.8% mom. That’s the fastest monthly growth since March 2021, and the ninth consecutive monthly expansion. Services-producing industries grew 0.9% while goods-producing industries grew 1.5%. 16- of industrial sectors expanded. Advance information indicates that GDP increased 0.5% mom in March.

ECB Lane: Scale and timing of interest normalization are data-dependent

ECB Chief Economist Philip Lane said in a Bloomberg TV interview, “The story is not the issue about are we going to move away from -0.5% for the deposit rate. The big issue which we do need to still be data-dependent about is the scale and the timing of interest-rate normalization.”

“In the near-term, yes, inflation is very high and that does carry its own risk of momentum,” Lane admitted. “On the other hand the high energy prices are eating into disposable incomes, it’s reducing consumption and the war has a scope – especially depending on how it goes – in terms of mapping into lower investment, lower consumption, confidence effects and extra pressure on energy.”

Eurozone CPI ticked up to 7.5% yoy in Apr, core CPI rose to 3.5% yoy

Eurozone CPI ticked up from 7.4% yoy to 7.5% yoy in April, matched expectations. CPI core rose from 2.9% yoy to 3.5% yoy, above expectation of 3.1% yoy. Looking at the main components of euro area inflation, energy is expected to have the highest annual rate in April (38.0%, compared with 44.4% in March), followed by food, alcohol & tobacco (6.4%, compared with 5.0% in March), non-energy industrial goods (3.8%, compared with 3.4% in March) and services (3.3%, compared with 2.7% in March).

Eurozone GDP grew 0.2% qoq in Q1, EU up 0.4% qoq

Eurozone GDP grew 0.2% qoq in Q1, slightly below expectation of 0.3% qoq. Comparing with the same quarter a year ago, Eurozone GDP grew 5.0% yoy.

EU GDP grew 0.4% qoq, 5.2% yoy. Among the Member States for which data are available for the first quarter 2022, Portugal (+2.6%) recorded the highest increase compared to the previous quarter, followed by Austria (+2.5%) and Latvia (+2.1%). Declines were recorded in Sweden (-0.4%) and in Italy (-0.2%). The year on year growth rates were positive for all countries.

Germany GDP grew 0.2% qoq in Q1, Ukraine war weighs on short-term development

Germany GDP grew 0.2% qoq in Q1, matched expectations. On the same quarter a year earlier, GDP grew 3.7% yoy. The growth was mainly due to higher capital formation, whereas the balance of exports and imports had a downward effect on economic growth. The economic consequences of the war in Ukraine have had a growing impact on the short-term economic development since late February.

France GDP stagnated in Q1 with sharp decline in household consumption

France GDP stagnated with 0.0% qoq growth in Q1, below expectation of 0.3% qoq. Households’ consumption expenditure sharply decreased (-1.3% after +0.6%) while gross fixed capital formation (GFCF) slightly decelerated (+0.2% after +0.3%). Finally, internal demand excluding inventory changes contributed to -0.6 points to GDP growth, after +0.5 points in the previous quarter.

Also from France, consumer spending dropped -1.3% mom in March, worse than expectation of -0.1% mom. CPI accelerated from 5.1% yoy to 5.4% yoy in April, above expectation of 5.1% yoy.

SNB Jordan: Swiss can withstand franc being stronger in nominal terms

SNB Chairman Thomas Jordan said two reasons have spoken against a rise in interest rate in reaction to inflation. “First, inflationary pressure is moderate here in Switzerland. Second, inflation is likely to return to the range compatible with price stability in the foreseeable future,” he said.

SNB forecasts inflation to average 2.1% this year before declining in 2023 and 2024. “The monetary conditions are therefore appropriate at present,” Jordan said. “However, should there be signs of a strengthening and spread in inflationary pressure, we will not hesitate to take the necessary measures.”

On Swiss Franc exchange rate, he said, it there had been “hardly any change in the real exchange rate” over the past few quarters. “We do not react mechanically to every instance of upward pressure,” he added. “If you have followed the Swiss franc closely over the past months, you will know that it has gradually appreciated and has at times even fallen below parity to the euro.”

Also, SNB had “quite deliberately” allowed appreciation of the Franc. “This means that our economy can withstand the franc being stronger in nominal terms,” Jordan said. “The higher prices abroad and the nominally stronger Swiss franc roughly balance one another out.”

Swiss KOF economic barometer rose to 101.7, contrast between corona easing and war

Swiss KOF Economic Barometer improved from 99.7 to 101.7 in April, above expectation of 99.3. It’s back above long-term average of 100 after dipping below that level in March. Outlook for the Swiss economy is therefore rather favorable in the short term.

KOF said, accommodation and food service activities and the other services sector are responsible for the rise. On the other hand, indicators for foreign demand are currently the strongest drag.

It added, “this contrast highlights the tension between Corona easing and international burdens, especially the Ukraine war.”

Also from Swiss, retail sales dropped -6.6% yoy in March, below expectation of 13.3% yoy rise.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0460; (P) 1.0512 (R1) 1.0553; More…

A temporary low is formed at 1.0470 with current recovery. Intraday bias in EUR/USD is turned neutral first, for consolidations. Upside of recovery should be limited by 1.0756 support turned resistance to bring fall resumption. On the downside, break of 1.0470 will resume larger down trend to 161.8% projection of 1.1494 to 1.0805 from 1.1184 at 1.0069.

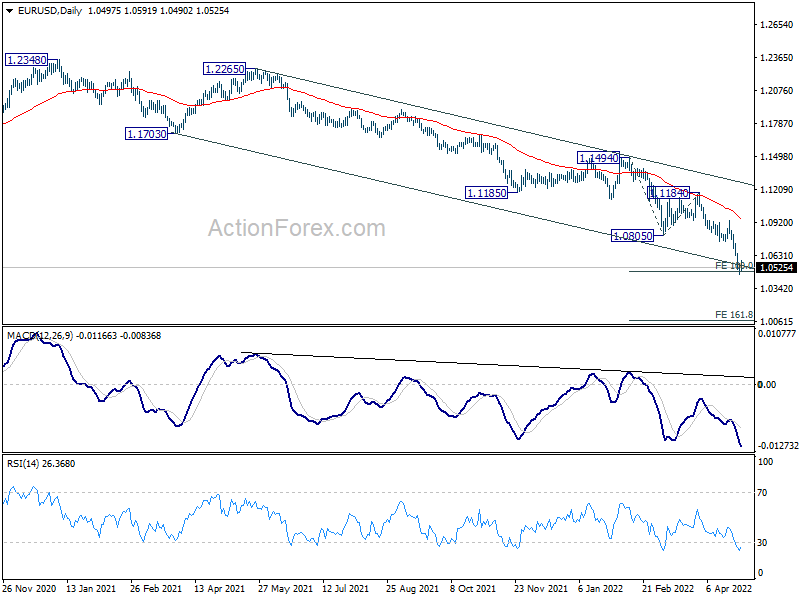

In the bigger picture, the decline from 1.2348 (2021 high) is expected to continue as long as 1.1185 support turned resistance holds. The break of 1.0635 (2020 low) now raises the chance that it’s resuming long term down trend from 1.6039 (2008 high). Retest of 1.0339 (2017 low) low should be seen next. Decisive break there will confirm this bearish case.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | Private Sector Credit M/M Mar | 0.40% | 0.60% | 0.60% | |

| 01:30 | AUD | PPI Q/Q Q1 | 1.60% | 1.50% | 1.30% | |

| 01:30 | AUD | PPI Y/Y Q1 | 4.90% | 4.20% | 3.70% | |

| 05:30 | EUR | France Consumer Spending M/M Mar | -1.30% | -0.10% | 0.90% | |

| 05:30 | EUR | France GDP Q/Q Q1 P | 0.00% | 0.30% | 0.70% | 0.80% |

| 06:00 | EUR | Germany Import Price Index M/M Mar | 5.70% | 3.20% | 1.30% | |

| 06:30 | CHF | Real Retail Sales Y/Y Mar | -6.60% | 13.30% | 12.80% | 12.50% |

| 07:00 | CHF | KOF Leading Indicator Apr | 101.7 | 99.3 | 99.7 | |

| 08:00 | EUR | Germany GDP Q/Q Q1 P | 0.20% | 0.20% | -0.30% | |

| 08:00 | EUR | Italy GDP Q/Q Q1 P | -0.20% | -0.20% | 0.60% | |

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Mar | 6.30% | 6.20% | 6.30% | 6.40% |

| 09:00 | EUR | Eurozone GDP Q/Q Q1 P | 0.20% | 0.30% | 0.30% | |

| 09:00 | EUR | Eurozone CPI Y/Y Apr P | 7.50% | 7.50% | 7.40% | |

| 09:00 | EUR | Eurozone CPI Core Y/Y Apr P | 3.50% | 3.10% | 2.90% | |

| 12:30 | CAD | GDP M/M Feb | 1.10% | 0.80% | 0.20% | |

| 12:30 | USD | Personal Income M/M Mar | 0.50% | 0.40% | 0.50% | 0.70% |

| 12:30 | USD | Personal Spending Mar | 1.10% | 0.60% | 0.20% | 0.60% |

| 12:30 | USD | PCE Price Index M/M Mar | 0.90% | 0.50% | 0.60% | 0.50% |

| 12:30 | USD | PCE Price Index Y/Y Mar | 6.60% | 6.50% | 6.40% | 6.30% |

| 12:30 | USD | Core PCE Price Index M/M Mar | 0.30% | 0.30% | 0.40% | 0.30% |

| 12:30 | USD | Core PCE Price Index Y/Y Mar | 5.20% | 5.30% | 5.40% | 5.30% |

| 12:30 | USD | Employment Cost Index Q1 | 1.40% | 1.10% | 1.00% | |

| 13:45 | USD | Chicago PMI Apr | 61.5 | 62.9 | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Apr F | 65.7 | 65.7 |