Products You May Like

The recovery in Dollar and Yen appeared to be rather short-lived, as overall risk sentiment was steady. FOMC minutes affirmed market expectations of 50bps rate hikes ahead, which is not news. That triggered little reaction in the greenback. As for today, Euro is regaining some ground together with Swiss Franc. New Zealand Dollar is the weaker one with Yen. But Dollar is staying as the worst performer for the week.

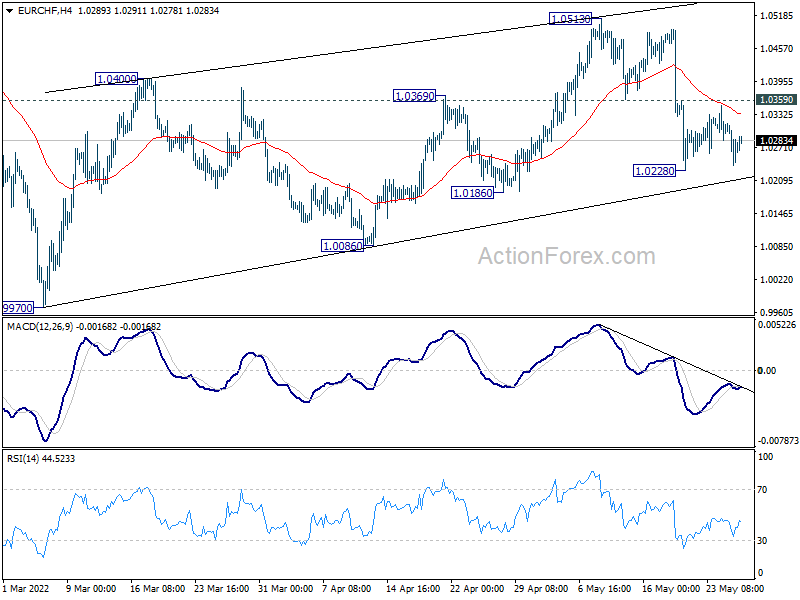

Technically, one focus is whether EUR/CHF would break through 1.0228 temporary low to resume the fall from 1.0513. If happens, that could set up EUR/CHF further fall back towards parity. That might also drag Euro down in other pairs, in particular EUR/JPY, which is still staying in the corrective pattern from 139.99.

In Asia, at the time of writing, Nikkei is up 0.08%. Hong Kong HSI is down -0.13%. China Shanghai SSE is up 0.65%. Singapore Strait Times is up 0.81%. Japan 10-year JGB yield is up 0.15 at 0.227. Overnight, DOW rose 0.60%. S&P 500 rose 0.95%. NASDAQ rose 1.51%. 10-year yield dropped -0.011 to 2.749.

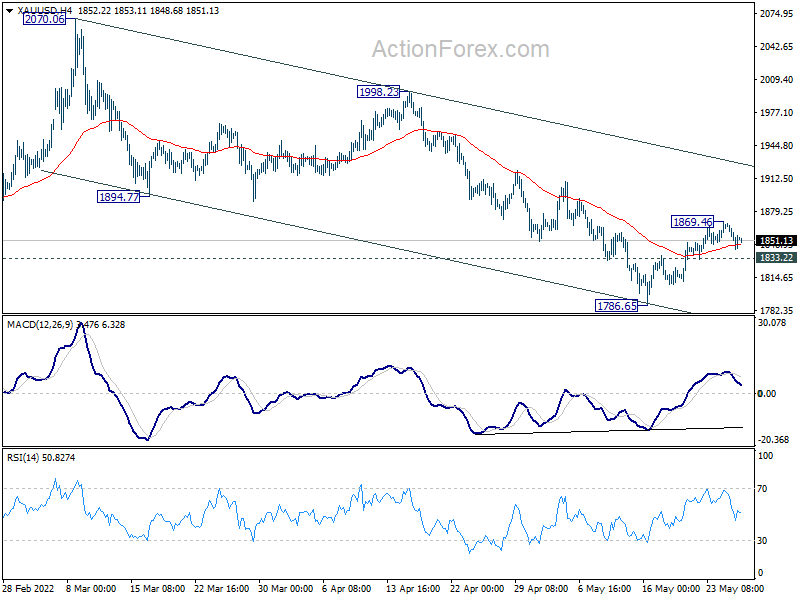

FOMC minutes affirms 50bps hikes ahead, Gold lost momentum

In the minutes of the May 3-4 FOMC minutes, Fed said, “most participants judged that 50 basis point increases in the target range would likely be appropriate at the next couple of meetings”. That is in-line with market expectations, and other communications from Fed officials, that the plan is set for 50bps hike per meeting for June and July at least.

Also, it’s noted, “at present, participants judged that it was important to move expeditiously to a more neutral monetary policy stance. They also noted that a restrictive stance of policy may well become appropriate depending on the evolving economic outlook and the risks to the outlook.”

Gold dips mildly after FOMC minutes, as recovery from 1786.65 lost momentum. For now, further rise could still be as long as 1833.22 minor support holds. Above 1869.46 will resume the rebound to channel resistance a around 1926. However, break of 1833.22 should resume the whole fall from 2070.06 high through 1786.65.

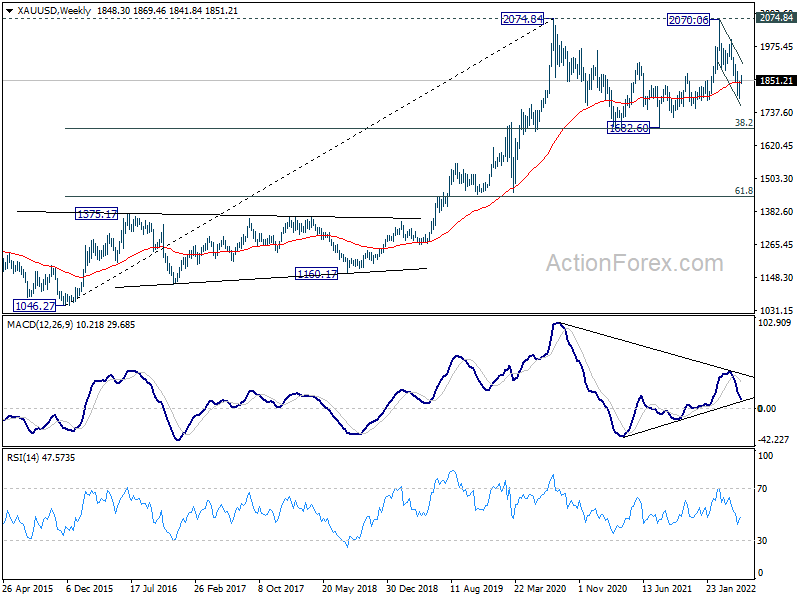

Overall, there is no change in the view that fall from 2070.06 is the third leg of the consolidation pattern from 2074.84. Deeper decline would be seen as the recovery completes, towards 1682.60 support.

RBNZ Orr: Single biggest risk is embedded inflation expectation

RBNZ Governor Adrian Orr told a parliamentary committee today, “the single biggest risk to this nation at the moment is enabling current high CPI inflation to become embedded in future ongoing inflation expectation.”

Orr said that a recession is not projected for New Zealand, even though he cannot rule it out. Challenges to growth were coming through significant downgrades to global growth, particularly China.

Looking ahead

The European calendar is empty today with France and Germany on holiday. Canada retail sales will be featured later in the day. US will release GDP revision, jobless claims and pending home sales.

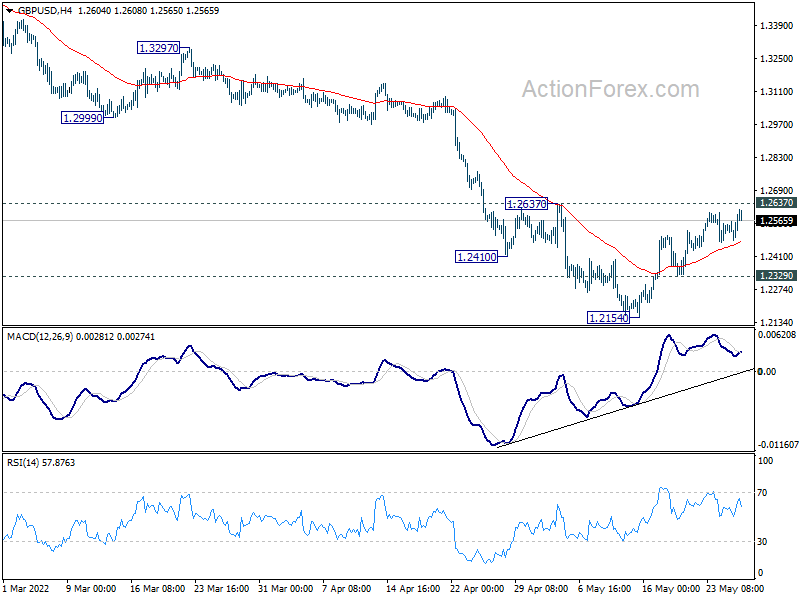

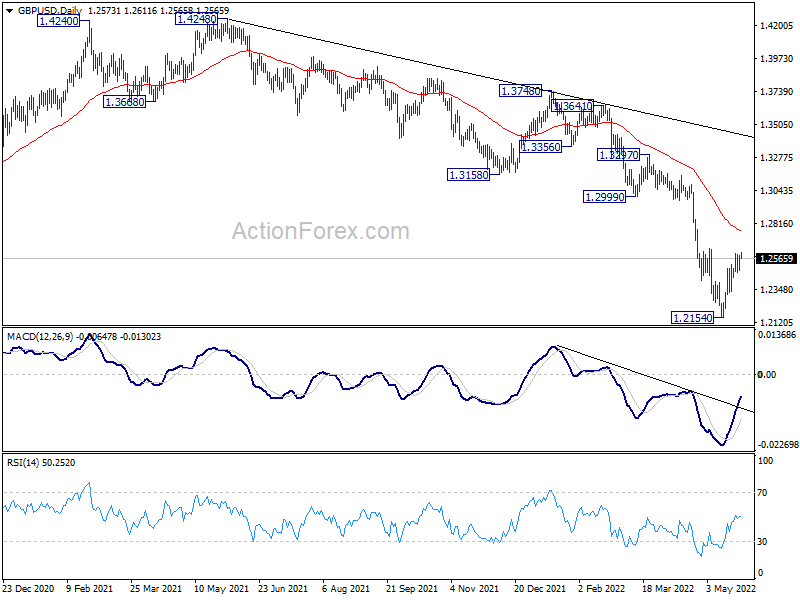

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2510; (P) 1.2551; (R1) 1.2620; More..

GBP/USD’s recovery from 1.2154 extends higher but stays below 1.2637 resistance. Intraday bias remains neutral for the moment. On the upside, firm break of 1.2637 resistance will bring stronger rebound to 55 day EMA (now at 1.2759). On the downside, below 1.2329 minor support will retain near term bearishness and bring retest of 1.2154 first. Break there will resume larger down trend from 1.4248.

In the bigger picture, based on current momentum, fall from 1.4248 (2018 high) at least at the same degree as the rise from 1.1409 (2020 low). That is, fall from 1.4248 could be a leg inside the pattern from 1.1409, or resuming the longer term down trend. In either case, deeper decline is expected as long as 1.2999 support turned resistance holds. Next target is 1.1409 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Corporate Service Price Index Y/Y Apr | 1.70% | 0.90% | 1.30% | |

| 01:30 | AUD | Private Capital Expenditure Q1 | -0.30% | 1.50% | 1.10% | 2.30% |

| 12:30 | CAD | Retail Sales M/M Mar | 1.50% | 0.10% | ||

| 12:30 | CAD | Retail Sales ex Autos M/M Mar | 2.20% | 2.10% | ||

| 12:30 | USD | Initial Jobless Claims (May 20) | 210K | 218K | ||

| 12:30 | USD | GDP Price Index Q1 P | 8.00% | 8.00% | ||

| 12:30 | USD | GDP Annualized Q1 P | -1.30% | -1.40% | ||

| 14:00 | USD | Pending Home Sales M/M Apr | -1.70% | -1.20% | ||

| 14:30 | USD | Natural Gas Storage | 83B | 89B |