Products You May Like

Dollar stays broadly pressured today and it’s set to end as the worst performer for the week. PCE data offered some hope that inflation has finally topped. Broad risk sentiment is steady as US stocks could extend rebound in the final session of the week. Benchmark treasury yields are also trading slightly lower. Buying focus has turned to commodity currencies today, as led by Aussie. European majors are also slightly weaker with Yen.

Technically, 1.2712 support in USD/CAD is an immediate focus, as WTI crude oil is also extending rally too. Break of 1.2712 will argue that rise from 1.2401 has completed at 1.3075. More importantly, that came after rejection by 1.3022 long term fibonacci resistance. Deeper fall could be seen back towards 1.2401, and rise the chance that whole rebound from 1.2005 has finished. That, if happens, would be a bad sign for the greenback.

In Europe, at the time of writing, FTSE is up 0.38%. DAX is up 1.01%. CAC is up 1.09%. Germany 10-year yield is down -0.051 at 0.945. Earlier in Asia, Nikkei rose 0.66%. Hong Kong HSI rose 2.89%. China Shanghai SSE rose 0.23%. Japan 10-year JGB yield dropped -0.0053 to 0.230.

US PCE inflation slowed to 6.3% yoy, core PCE down to 4.9% yoy

US personal income rose 0.5% mom, or USD 89.3B, in April, below expectation of 0.6% mom. Personal spending rose 0.9% mom, or USD 152.3B, above expectation of 0.7% mom.

Headline PCE price index slowed from 6.6% yoy to 6.3% yoy, below expectation of 6.6% yoy. Core PCE price index slowed from 5.2% yoy to 4.9% yoy, matched expectations. Energy prices rose 30.4% yoy while food prices rose 10.0% yoy.

Bundesbank Nagel: We must make the first rates move in July

In a Der Spiegel interview, Bundesbank President Joachim Nagel said, “in our June meeting we must send a clear signal where we’re going. From my current perspective, we must then make the first rates move in July and have others follow in the second half of the year.”

Earlier this week, ECB President Christine Lagarde has already indicated, “we’re moving (deposit rate) very likely into positive territory at the end of the third quarter… When you’re out of negative (rates) you can be at zero, you can be slightly above zero. This is something that we will determine on the basis of our projections and … forward guidance.”

BoJ Kuroda: Prices won’t rise sustainably without wage hikes

BoJ Governor Haruhiko Kuroda told the parliament today that core inflation (all items excluding fresh food) is “likely to remain around 2% for about 12 months”, unless energy prices drop sharply.

However, he emphasized that “prices won’t rise sustainably, stably unless accompanied by wage hikes.” That’s seen as in indication that recent rise in inflation is not enough to lead to exit of the ultra-loose monetary policy.

Also from Japan, Tokyo CPI core was unchanged at 1.9% yoy in May, below expectation of 2.0% yoy.

Australia retail sales rose 0.9% mom in Apr, driven by higher food prices

Australia retail sales rose 0.9% mom in April, slightly below expectation of 1.0% mom. For the 12-month period, sales rose 9.6% yoy.

New South Wales was the only state or territory to record a fall, down -0.3%. Queensland had the largest rise in retail turnover, up 1.6%. Turnover also rose in Victoria (1.1%), Western Australia (2.2 %), South Australia (1.4%), Tasmania (2.0%), the Australian Capital Territory (0.5%) and the Northern Territory (0.7%).

ABS said: “The strength in retail turnover is being driven by spending across the food industries. High food prices have combined with increased household spending over the April holiday period as more people are travelling, dining out and holding family gatherings.

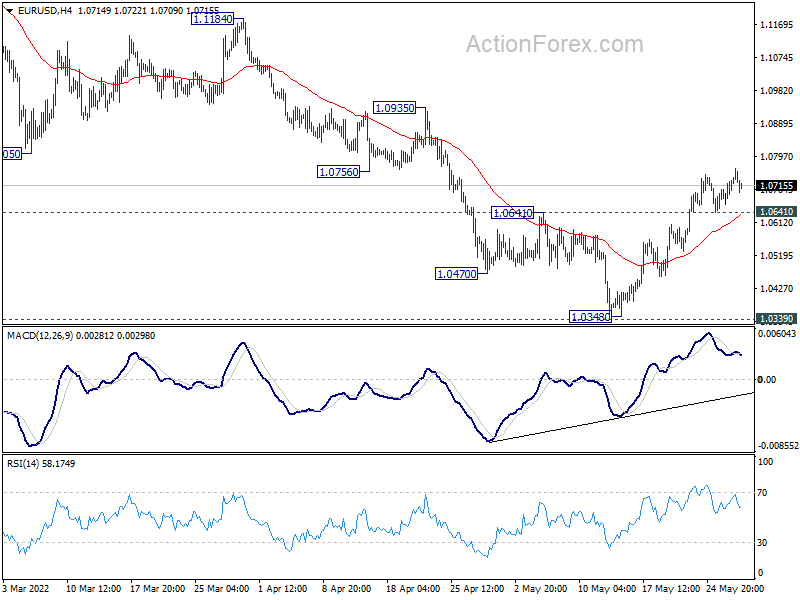

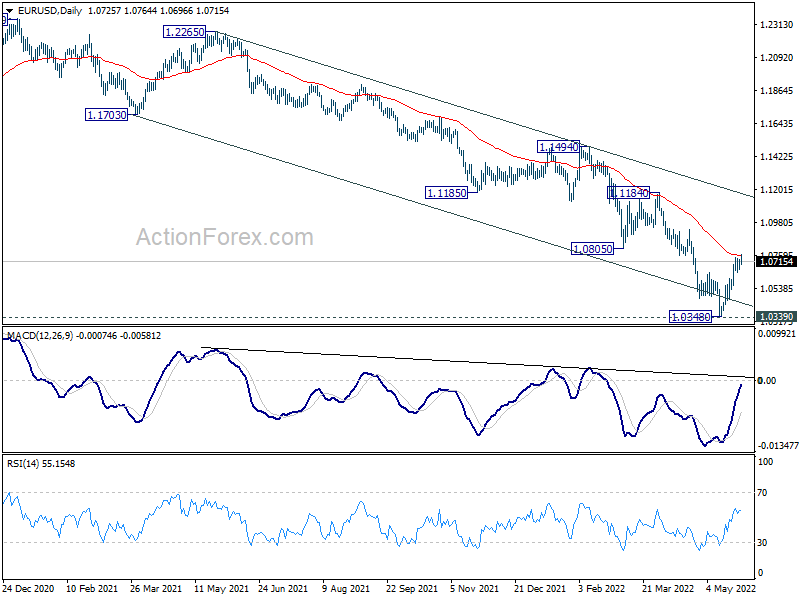

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0685; (P) 1.0709 (R1) 1.0755; More…

Intraday bias in EUR/USD stays mildly on the upside, as rebound from 1.0348 is in progress. Firm break of 55 day EMA (now at 1.0758) will target 1.0935 resistance next. On the downside, however, break of 1.641 minor support will turn bias back to the downside for retesting 1.0348 low instead.

In the bigger picture, focus stays on 1.0339 long term support (2017 low). Decisive break there will resume whole down trend from 1.6039 (2008 high). Next target is 61.8% projection of 1.3993 to 1.0339 from 1.2348 at 1.0090. However, firm break of 1.0805 support turned resistance will delay this bearish case and bring medium term corrective rebound first.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Core Y/Y May | 1.90% | 2.00% | 1.90% | |

| 01:30 | AUD | Retail Sales M/M Apr | 0.90% | 1.00% | 1.60% | |

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Apr | 6.00% | 6.30% | 6.30% | |

| 12:30 | USD | Personal Income M/M Apr | 0.40% | 0.60% | 0.50% | |

| 12:30 | USD | Personal Spending Apr | 0.90% | 0.70% | 1.10% | 1.40% |

| 12:30 | USD | PCE Price Index M/M Apr | 0.20% | 0.80% | 0.90% | |

| 12:30 | USD | PCE Price Index Y/Y Apr | 6.30% | 6.60% | 6.60% | |

| 12:30 | USD | Core PCE Price Index M/M Apr | 0.30% | 0.40% | 0.30% | |

| 12:30 | USD | Core PCE Price Index Y/Y Apr | 4.90% | 4.90% | 5.20% | |

| 12:30 | USD | Goods Trade Balance (USD) Apr P | -105.9B | -114.8B | -127.1B | -125.9B |

| 12:30 | USD | Wholesale Inventories Apr P | 2.10% | 2.00% | 2.30% | 2.70% |

| 14:00 | USD | Michigan Consumer Sentiment Index May F | 59.1 | 59.1 |