Products You May Like

Yen, Swiss Franc and Dollar turn softer with other markets trading in slightly upbeat tone. Traders are back to business as usual, after no substantial actions from China during the time US House Speaker Nancy Pelosi visited Taiwan. Australian Dollar is leading Canadian and Sterling higher. Euro is mixed for now. Focuses will turn to BoE rate decision tomorrow.

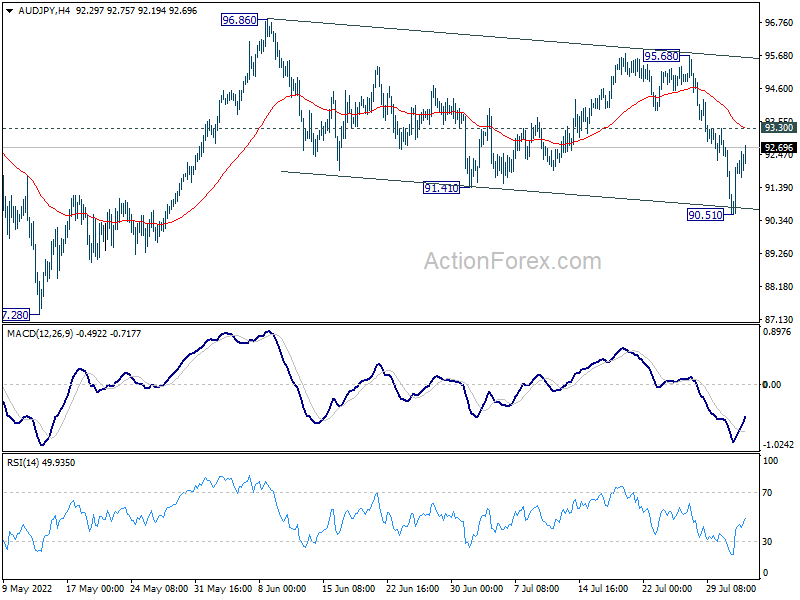

Technically, one focus is now on AUD/JPY to gauge the chance of resumption in risk-on trades. Break of 93.30 minor resistance will argue that whole corrective pattern from 96.86 has completed with three waves down to 90.51. Further rally would be seen back to 95.68 resistance first. Break will argue that medium term up trend is ready to resume.

In Europe, at the time of writing, FTSE is up 0.16%. DAX is up 0.22%. CAC is up 0.40%. Germany 10-year yield is up 0.065. Earlier in Asia, Nikkei rose 0.53%. Hong Kong HSI rose 0.40%. China Shanghai SSE dropped -0.71%. Singapore Strait Times rose 0.40%. Japan 10-year JGB yield rose 0.0130 to 0.190.

Eurozone retail sales dropped -1.2% mom in Jun, EU down -1.3% mom

Eurozone retail sales dropped -1.2% mom in June versus expectation of 0.1% mom rise. The volume of retail trade decreased by -2.6% mom for non-food products, by -1.1% for automotive fuels mom and by -0.4% mom for food, drinks and tobacco.

EU retail sales dropped -1.3% mom. Among Member States for which data are available, the largest monthly decreases in the total retail trade volume were registered in Denmark (-3.8%), the Netherlands (-3.4%) and Estonia (-2.4%). Increases were observed in Ireland and Malta (both +0.5%), Finland (+0.3%) and Austria (+0.2%).

Eurozone PPI up 1.1% mom, 35.8% yoy in Jun

Eurozone PPI rose 1.1% mom, 35.8% yoy in June, versus expectation of 1.0% mom, 35.7% yoy. For the month, Industrial producer prices increased by 2.7% mom in the energy sector, by 0.7% mom for durable consumer goods and non-durable consumer goods and by 0.4% mom for intermediate goods and for capital goods. Prices in total industry excluding energy increased by 0.4% mom.

EU PPI rose 1.3% mom, 36.1% yoy. The highest monthly increases in industrial producer prices were recorded in Ireland (+13.2%), Lithuania (+5.2%) as well as Latvia and Finland (both +4.0%). Decreases were observed in Greece (-3.2%) and Luxembourg (-2.2%).

Eurozone PMI composite finalized at 49.9, outlook darkened, signalling July GDP contraction

Eurozone PMI Services was finalized at 51.2 in July, down from 53.0 in June. That’s the lowest level in 6 months. PMI Composite was finalized at 49.9, down from 52.0 in June, a 17-month low.

Looking at some member states, Spain PMI Composite was finalized at 52.7 (6-month low), France at 51.7 (15-month low), Germany at 48.1 (25-month low), and Italy at 47.7 (18-month low).

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence said: “The eurozone economic outlook has darkened at the start of the third quarter, with the latest survey data signalling a contraction of GDP in July. Soaring inflation, rising interest rates and supply worries – notably for energy – have led to the biggest drops in output and demand seen for a almost a decade, barring pandemic lockdown months.

UK PMI services finalized at 52.6, composite at 52.1

UK PMI Services was finalized at 52.6 in July, down from June’s 54.3, worst reading in 17 months. PMI Composite was finalized at 52.1, down from 53.7 in June, the lowest rate of expectation since February 2021.

Tim Moore, Economics Director at S&P Global Market Intelligence: “UK service providers reported their worst month for business activity expansion since the national lockdown in February 2021. Reduced levels of discretionary consumer spending and efforts by businesses to contain expenses due to escalating inflation have combined to squeeze demand across the service economy. The near-term outlook also looks subdued, as new order growth held close to June’s 16-month low and business optimism was the second weakest since May 2020.

Swiss CPI unchanged at 3.4% yoy in Jul, core CPI ticked up to 1.8% yoy

Swiss CPI was unchanged at 3.4% yoy in July, below expectation of 3.6% yoy. Core CPI rose from 1.9% yoy to 2.0% yoy. Domestic products inflation rose from 1.7% yoy to 1.8% yoy. Imported products inflation dropped from 8.5% yoy to 8.4% yoy.

FSO said: “The stability of the index compared with the previous month is the result of opposing trends that counterbalanced each other overall. Prices for heating oil decreased, as did those for clothing and footwear due to seasonal sales. In contrast, prices for gas and supplementary accommodation increased.”

Australia AiG construction dropped to 45.3, RBA tightening will end the boom

Australia AiG Performance of Construction Index dropped -0.9 to 45.3 in July. Activity dropped -3.5 to 42.7. Employment rose 2.2 to 53.0. New orders dropped -2.7 to 43.1. Supplier deliveries rose 3.2 to 42.2. Input prices dropped -2.2 to 93.8. Selling prices rose 4.4 to 87.1.

HIA Economist, Thomas Devitt, said: “Confidence in the housing sector has been adversely impacted by rising rates which will compound the rise in the cost of construction. This has not yet materialised in slowing sales or approvals of new homes and there is still a large volume of building work in the pipeline to complete. Recent declines in confidence, as shown in this month’s Australian PCI, reflect an anticipation on the part of builders of less new work entering the pipeline in coming months as the RBA’s current tightening cycle will, inevitably, bring an end to the boom.”

New Zealand employment flat in Q2, wage grow strongest since 2008

New Zealand employment was essentially flat in Q2, below expectation of 0.4% rise. Unemployment rate ticked up from 3.2% to 3.3%, against expectation a fall to 3.1%. Labor force participation rate dropped -0.1% to 70.8%.

Wage inflation (salary and wage rates, including overtime) in all sectors rose 1.1% qoq, 3.5% yoy. It grew 1.3% qoq, 3.4% yoy in private sector, and 0.6% qoq, 3.0% yoy in public sector.

“Measures of spare labour market capacity have fallen over the year and remained low for several quarters, continuing to show a tight labour market,” work and wellbeing statistics senior manager Becky Collett said.

“The June quarter had the largest increase in LCI salary and wages rates since late-2008. Over the year, a steadily increasing number of wages have been raised to better match market rates, as well as attracting or retaining staff,” business employment insights manager Sue Chapman said.

China Caixin PMI services rose to 55.5, composite dropped to 54.0

China Caixin PMI Services rose from 54.5 to 55.5 in July, above expectation of 54.0. That’s the highest level since April 2021. PMI Composite dropped from 55.3 to 54.0.

Wang Zhe, Senior Economist at Caixin Insight Group said: “In general, the eased Covid situation and restrictions facilitated a continuous recovery in the economy. The services sector, which had been previously hit harder by the outbreaks than manufacturing, showed stronger improvement. Supply and demand continued to improve with supply stronger than demand. The labor market shrank greatly, adding to employment pressures. Business costs steadily climbed while prices charged remained stable, posing challenges for company profits. The market held on to positive sentiment, even with concerns about the outlook for Covid and the economy.”

Looking ahead

Germany trade balance, Swiss CPI, Eurozone PMI services final, PPI and retail sales, and UK PMI services final will be released in European session. Later in the day, US will release ISM services and factory orders.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 131.33; (P) 132.25; (R1) 134.10; More…

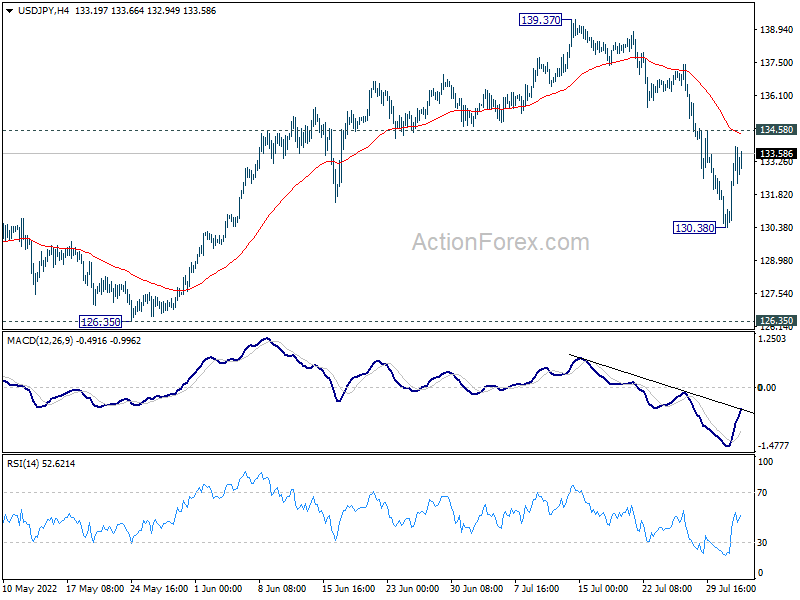

Intraday bias in USD/JPY remains neutral and some consolidations would be seen above 130.38 first. On the downside, below 130.38 will resume the fall from 139.37, as a correction to medium term uptrend, towards 126.35 support. Strong support is expected above there, at least on first attempt, to bring rebound. On the upside, firm break of 134.58 will turn bias to the upside for stronger rally to retest 139.37 high.

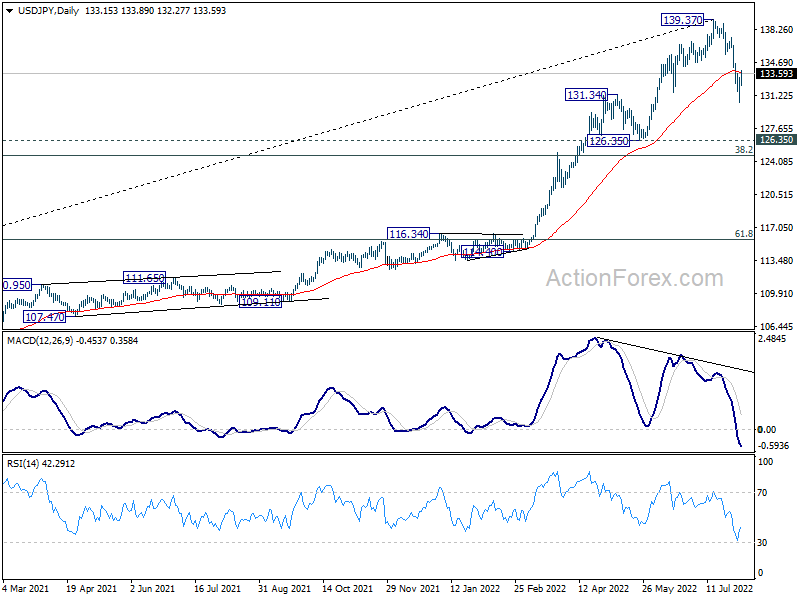

In the bigger picture, a medium term top should be in place at 139.37, on bearish divergence condition in daily MACD. Fall from there could be correcting whole up trend from 101.18 (2020 low). While deeper decline cannot be ruled out, outlook will stays bullish as long as 55 week EMA (now at 121.84) holds. Long term up trend is expected to resume through 139.37 at a later stage, after the correction finishes.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | AUD | AiG Performance of Construction Index Jul | 45.3 | 46.2 | ||

| 22:45 | NZD | Employment Change Q2 | 0.00% | 0.40% | 0.10% | |

| 22:45 | NZD | Unemployment Rate Q2 | 3.30% | 3.10% | 3.20% | |

| 22:45 | NZD | Labour Cost Index Q/Q Q2 | 1.30% | 1.10% | 0.70% | |

| 01:45 | CNY | Caixin Services PMI Jul | 55.5 | 54 | 54.5 | |

| 06:00 | EUR | Germany Trade Balance (EUR) Jun | 6.4B | -1.1B | -1.0B | |

| 06:30 | CHF | CPI M/M Jul | 0.00% | 0.00% | 0.50% | |

| 06:30 | CHF | CPI Y/Y Jul | 3.40% | 3.60% | 3.40% | |

| 07:45 | EUR | Italy Services PMI Jul | 48.4 | 50 | 51.6 | |

| 07:50 | EUR | France Services PMI Jul F | 53.2 | 52.1 | 52.1 | |

| 07:55 | EUR | Germany Services PMI Jul F | 49.7 | 49.2 | 49.2 | |

| 08:00 | EUR | Eurozone Services PMI Jul F | 51.2 | 50.6 | 50.6 | |

| 08:00 | EUR | Italy Retail Sales M/M Jun | -1.10% | 0.20% | 1.90% | 2.00% |

| 08:30 | GBP | Services PMI Jul F | 52.6 | 53.3 | 53.3 | |

| 09:00 | EUR | Eurozone PPI M/M Jun | 1.10% | 1.00% | 0.70% | 0.50% |

| 09:00 | EUR | Eurozone PPI Y/Y Jun | 35.80% | 35.70% | 36.30% | 36.20% |

| 09:00 | EUR | Eurozone Retail Sales M/M Jun | -1.20% | 0.10% | 0.20% | 0.40% |

| 13:45 | USD | Services PMI Jul F | 47 | 47 | ||

| 14:00 | USD | ISM Services PMI Jul | 53.5 | 55.3 | ||

| 14:00 | USD | Factory Orders M/M Jun | 0.80% | 1.60% | ||

| 14:30 | USD | Crude Oil Inventories | -1.4M | -4.5M |