Products You May Like

Euro is extending near term rally against Swiss Franc and Sterling after even higher than expected record inflation. But it’s struggling to gain against most other currencies. Dollar is also sluggish after ADP employment disappointment, while Yen’s is recovering. Commodity currencies are mixed for now. It seems like traders would continue to hold their bets until US non-farm payroll employment data.

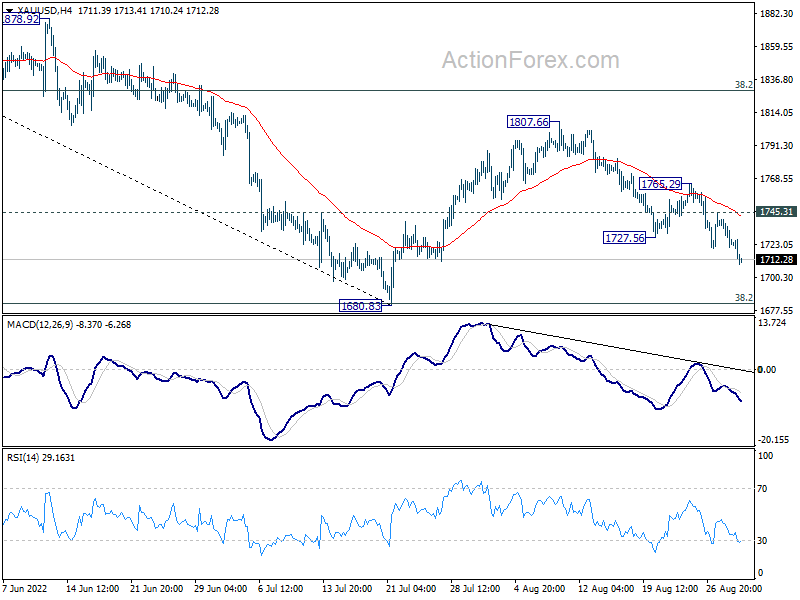

Technically, Gold’s decline continues after brief recovery and it’s on track to retest 1680.83 support holds. The question remains on whether this long term cluster support level would hold. Or, this level would be taken out decisively to complete confirm a long term trend reversal. In the latter case, it could be used as a confirmation for Dollar’s up trend resumption, in particular against Euro.

In Europe, at the time of writing, FTSE is down -0.86%. DAX is up 0.02%. CAC is down -0.24%. Germany 10-year yield is up 0.049 at 1.557. Earlier in Asia, Nikkei dropped -0.37%. Hong Kong HSI rose 0.03%. China Shanghai SSE dropped -0.78%. Singapore Strait Times dropped -0.55%. Japan 10-year JGB yield rose 0.0027 to 0.230.

US ADP employment grew 132k, a shift towards more conservative hiring pace

US ADP private employment grew 132k in August, well below expectation of 300k. By sector, goods-producing jobs grew 23k. Services-providing jobs grew 110k. By company size, small businesses added 25k jobs, medium added 53k, large added 54k. Annual pay was up 7.6%.

“Our data suggests a shift toward a more conservative pace of hiring, possibly as companies try to decipher the economy’s conflicting signals,” said Nela Richardson, chief economist, ADP. “We could be at an inflection point, from super-charged job gains to something more normal.”

Fed Mester expects rates above 4% by early next year, and hold it there

Cleveland Fed President Loretta Mester said, “my current view is that it will be necessary to move the fed funds rate up to somewhat above 4 percent by early next year and hold it there; I do not anticipate the Fed cutting the fed funds rate target next year.” “It would be a mistake to declare victory over the inflation beast too soon. Doing so would put us back in the stop-and-go monetary policy world of the 1970s, which was very costly to households and businesses,” she added.

Canada GDP grew 0.1% mom in Jun, but to contract -0.1% mom in Jul

Canada GDP grew 0.1% mom in June, matched expectations. Services-producing industries grew 0.2% mom while goods- producing industries rose 0.1% mom. 14 of 20 industrial sectors expanded in the month.

Advance information indicates that real GDP edged down by -0.1% mom in July. Output was down in the manufacturing, wholesale, retail trade and utilities sectors. Declines were partly offset by increases in the mining, quarrying, oil and gas sector and the agriculture, forestry, fishing and hunting sector.

Eurozone CPI rose to 9.1% yoy in Aug, core CPI up to 4.3% yoy

Eurozone CPI accelerated further from 8.9% yoy to 9.1% yoy in August, above expectation of 9.0%. CPI core (all items excluding energy, food, alcohol, and tobacco) rose from 4.0% yoy to 4.3% yoy, above expectation of 4.0% yoy.

Looking at the main components, energy is expected to have the highest annual rate in August (38.3%, compared with 39.6% in July), followed by food, alcohol & tobacco (10.6%, compared with 9.8% in July), non-energy industrial goods (5.0%, compared with 4.5% in July) and services (3.8%, compared with 3.7% in July).

France goods consumption volume dropped -0.8% mom in Jul, CPI slowed to 5.8% yoy in Aug

France household consumption in goods, in volume, dropped -0.8% mom in July. The decline was mainly due to further decrease of consumption of manufactured goods (–1.4% after –0.7%). Food consumption also decreased further (–0.4% after –0.3%). Energy consumption fell back (–0.4% after +2.7% in June).

All item CPI slowed from 6.1% yoy to 5.8% yoy in August. Food inflation rose from 6.8% yoy to 7.7% yoy. Energy inflation slowed from 28.5% yoy to 22.2% yoy. Manufactured products inflation rose from 2.7% yoy to 3.5% yoy. Services inflation was unchanged at 3.9% yoy.

BoJ Nakagawa: laid out three reasons for continuing powerful monetary easing

BoJ board member Junko Nakagawa said in a speech that it’s “necessary for the Bank of Japan to persistently continue with the current powerful monetary easing,” and she laid out three reasons for that.

Firstly, Japan is “still on its way to recovery” from the pandemic. “As demand remains insufficient compared with supply capacity, a shift in the direction of monetary policy toward tightening would likely drag down the economy and put significant downward pressure on the economic activity of firms and households.”

Secondly, current inflation in Japan “differ considerably in terms of degree and the number of items” comparing to those in the US and Europe. The difference is “likely due to the disparity in wage inflation”.

Thirdly, the 2% inflation target “needs to be achieved in a sustainable and stable manner”. “Even if the higher price of some items pushes up the overall price level to 2 percent, unless household disposable income increases, spending on products and services will decline due to budget constraints.” Japan is only “halfway to achieve the price stability target.

Japan industrial production rose 1.0% mom in Jul, auto jumped 12%

Japan industrial production grew 1.0% mom in July, way better than expectation of -0.5% mom decline. The Ministry of Economy, Trade and Industry maintained its output assessment, “fluctuates indecisively” reflecting the ups and downs in production in recent months.

Six of the 15 industries reported output increases while eight declined. The auto industry saw the biggest increase by sector, by 12.0% mom.

Based on a poll of manufacturers, the ministry expects industrial output to grow 5.5 percent in August and rise 0.8 percent in September.

Also released, retail trade rose 2.4% yoy in July, above expectation of 1.9% yoy. Housing starts dropped -5.4% yoy in July, worse than expectation of -3.4% yoy. Consumer confidence improved from 30.2 to 32.5 in August.

NZ ANZ business confidence improved to -47.8 in Aug

New Zealand ANZ Business Confidence rose from -56.7 to -47.8 in August. Own Activity Outlook rose from -8.7 to -4.0. Export intentions rose from -2.7 to 3.9. Investment intentions rose from -2.6 to -2.0. Employment intentions rose from 1.1 to 3.4. Pricing intentions dropped from 74.0 to 70.1. Cost expectations dropped from 91.3 to 90.9. Inflation expectations dropped slightly from 6.23 to 6.13.

ANZ said: “It would make sense that with inflation and wage inflation running so high, the neutral Official Cash Rate is creeping higher, meaning the sting of a given interest rate wears off. Risks are tilted towards the RBNZ having to continue on with OCR hikes next year to cool the economy sufficiently to feel comfortable they’re getting on top of the inflation problem.

China PMI manufacturing rose to 49.4 in Aug, contraction continued

China’s official PMI Manufacturing rose slightly from 49.0 to 49.4 in August, above expectation of 49.2. New orders ticked up from 48.5 to 49.2. Production was flat at 49.8. PMI Non-Manufacturing dropped from 53.8 to 52.6, above expectation of 52.2. PMI Composite dropped from 52.5 to 51.7.

The data showed manufacturing activity contracted for the second straight month. Also, the sector has been in contraction for five out of the past six months, briefly hitting 50.2 in June.

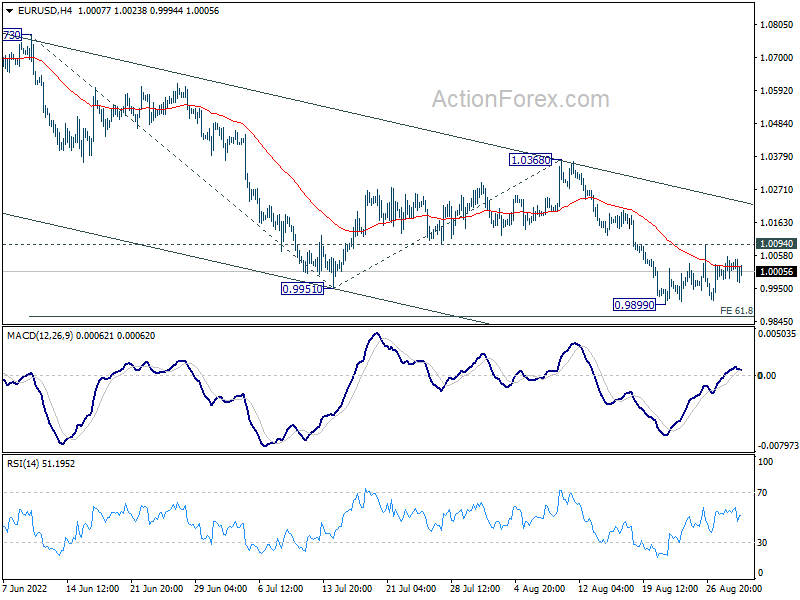

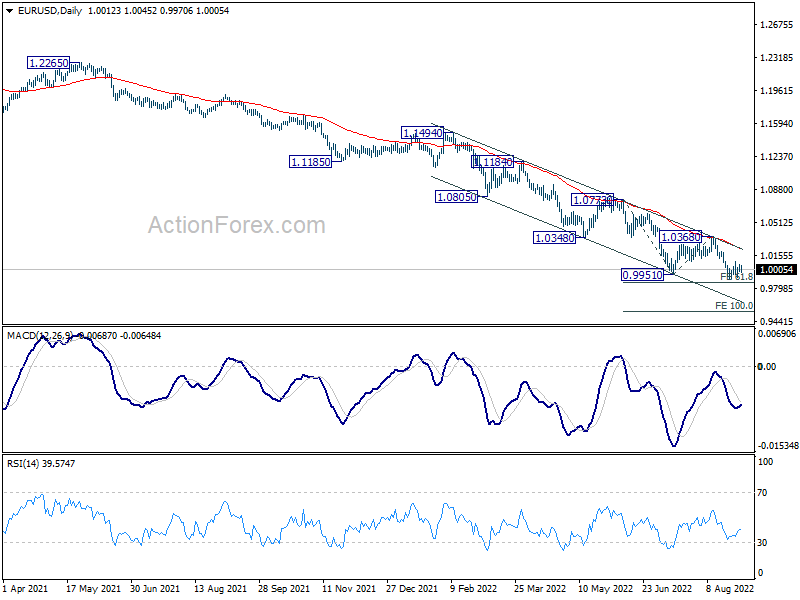

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 0.9980; (P) 1.0018; (R1) 1.0053; More…

Intraday bias in EUR/USD stays neutral as range trading continues, and further decline is expected with 1.0094 resistance intact. On the downside, break of 0.9899 will resume larger down trend to 61.8% projection of 1.0773 to 0.9951 from 1.0368 at 0.9860. Firm break there should prompt downside acceleration to 100% projection at 0.9546. However, firm break of 1.0094 minor resistance will dampen this bearish view, and turn bias back to the upside for 1.0368 resistance instead.

In the bigger picture, down trend from 1.6039 (2008 high) is still in progress. Next target is 100% projection of 1.3993 to 1.0339 from 1.2348 at 0.8694. In any case, outlook will stay bearish as long as 1.0368 resistance holds, in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Building Permits M/M Jul | 5.00% | -2.30% | -2.20% | |

| 23:01 | GBP | BRC Shop Price Index Y/Y Jul | 5.10% | 4.40% | ||

| 23:50 | JPY | Industrial Production M/M Jul P | 1.00% | -0.50% | 9.20% | 9.20% |

| 23:50 | JPY | Retail Trade Y/Y Jul | 2.40% | 1.90% | 1.50% | |

| 01:00 | NZD | ANZ Business Confidence Aug | -47.8 | -56.7 | ||

| 01:30 | CNY | NBS Manufacturing PMI Aug | 49.4 | 49.2 | 49 | |

| 01:30 | CNY | Non-Manufacturing PMI Aug | 52.6 | 52.2 | 53.8 | |

| 01:30 | AUD | Private Sector Credit M/M Jul | 0.70% | 0.70% | 0.90% | |

| 01:30 | AUD | Construction Work Done Q2 | -3.80% | 0.80% | -0.90% | -0.30% |

| 05:00 | JPY | Housing Starts Y/Y Jul | -5.40% | -3.40% | -2.20% | |

| 05:00 | JPY | Consumer Confidence Index Aug | 32.5 | 29.4 | 30.2 | |

| 06:00 | EUR | Germany Import Price Index M/M Jul | 1.40% | 1.60% | 1.00% | |

| 06:45 | EUR | France Consumer Spending M/M Jul | -0.80% | -0.30% | 0.10% | |

| 06:45 | EUR | France GDP Q/Q Q2 | 0.50% | 0.50% | 0.50% | |

| 07:55 | EUR | Germany Unemployment Change Aug | 28K | 27K | 48K | |

| 07:55 | EUR | Germany Unemployment Rate Aug | 5.50% | 5.50% | 5.40% | |

| 08:00 | CHF | Credit Suisse Economic Expectations Aug | -56.3 | -57.2 | ||

| 09:00 | EUR | Eurozone CPI Y/Y Aug P | 9.10% | 9.00% | 8.90% | |

| 09:00 | EUR | Eurozone CPI Core Y/Y Aug P | 4.30% | 4.00% | 4.00% | |

| 12:15 | USD | ADP Employment Change Aug | 132K | 300K | 128K | |

| 12:30 | CAD | GDP M/M Jun | 0.10% | 0.10% | 0.00% | |

| 13:45 | USD | Chicago PMI Aug | 53.2 | 52.1 | ||

| 14:30 | USD | Crude Oil Inventories | -0.4M | -3.3M |