Products You May Like

Trading in the currency market is rather subdued today and markets will stay quiet with US and Canada on holiday. Dollar is paring some of last week’s large losses but upside momentum is weak. On the other hand, Australia Dollar is turning slightly weaker as tomorrow’s RBA policy decision is awaited. The reaction in Aussie could be wild as it’s unknown whether RBA would maintain the tapering plan, or delay it, or reverse and increase in.

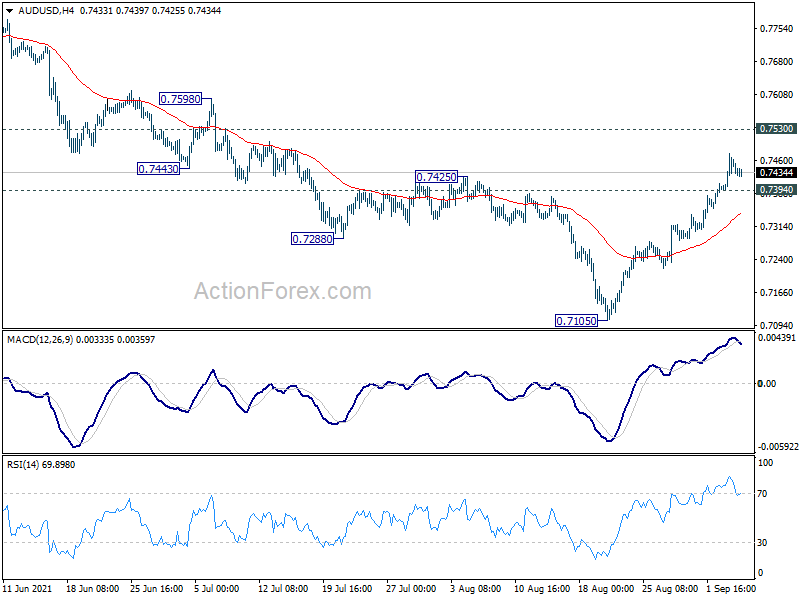

Technically, we’d pay attention to AUD/USD in the upcoming Asian session. As long as 0.7394 minor support holds, we’d expect rise form 0.7105 to extend to 0.7530 support turned resistance. Sustained break there would open the bullish case for retesting 0.8006 high. However, break of 0.7394 minor support will mix up the near term outlook and bring pull back first.

Suggested reading on RBA:

In Europe, at the time of writing, FTSE is up 0.66%. DAX is up 0.75%. CAC is up 0.82%. Germany 10-year yield is up 0.0027 at -0.354. Earlier in Asia, Nikkei rose 1.83%. Hong Kong HSI rose 1.01%. China Shanghai SSE rose 1.12%. Singapore Strait Times rose 0.56%.

Eurozone Sentix investor confidence dropped to 19.6, glowing global recovery

Eurozone Sentix Investor Confidence dropped to 19.6 in September, down from 22.2, slightly below expectation of 19.7. That’s the fourth decline in a row and the lowest reading since April, 2021. Current situation index was unchanged at 30.8. Expectations index dropped from1 4.0 to 9.0, lowest since May 2020.

Sentix said: “The momentum of the global economy is slowing. The expectation scores of most regions in the sentix business cycle indices are falling for the fourth or fifth time in a row. The expectation values are still positive, but the zenith of the economic recovery since the lockdowns last autumn has been passed. This is also evident in the assessments of the economic situation, which have only improved slightly in a few regions. In the important region of Asia ex Japan, on the other hand, we measure a noticeable decline”.

From Germany, factory orders rose 3.4% mom in July, well above expectation of -1.0% mom.

UK PMI construction dropped to 55.2 in Aug, begins to feel the impact of supply chain disruption

UK PMI Construction dropped to 55.2 in August, down from July’s 58.7, below expectation of 56.9. Markit said new order growth eased to a five-month low. All three monitored segments recorded softer rise in activity. But rise in input prices was second-fastest amid severe supply chain disruption.

Usamah Bhatti, Economist at IHS Markit: “Evidence that the UK construction sector began to feel the impact of ongoing supply chain disruption was widespread midway through the third quarter of 2021. Growth rates for overall activity as well as the three monitored subsectors eased further from the recent highs earlier in the summer. Similarly, new business inflows have continued to increase at a marked pace, yet even here the rate of growth has eased to a five-month low.

Nikkei closed up 1.83%, heading to 30714 high

Nikkei closed up strongly by adding 531.78 pts or 1.83% today, and the near term development is looking rather bullish. The corrective pattern from 30714.52 has likely completed at 26954.81. Further rise is now expected as long as this week’s gap is not covered. Next target is 30714.52 high.

Medium term development is also bullish with strong support seen from 55 week EMA. A market friendly result of next week’s leadership election of the ruling Liberal Democratic Party of Japan would probably pop Nikkei through 30714.53 high. In that case, the long term up trend would extend to 38.2% projection of 16358.19 to 30714.52 from 26954.81 at 32438.92 next.

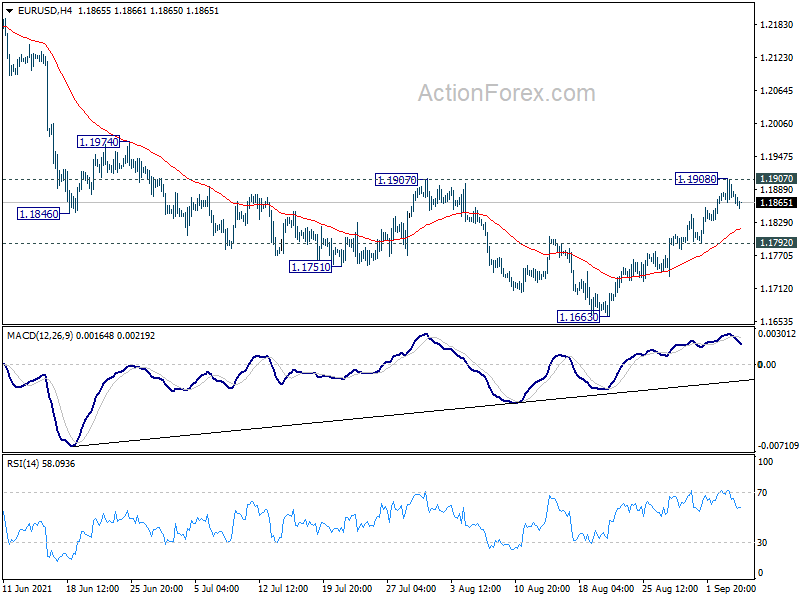

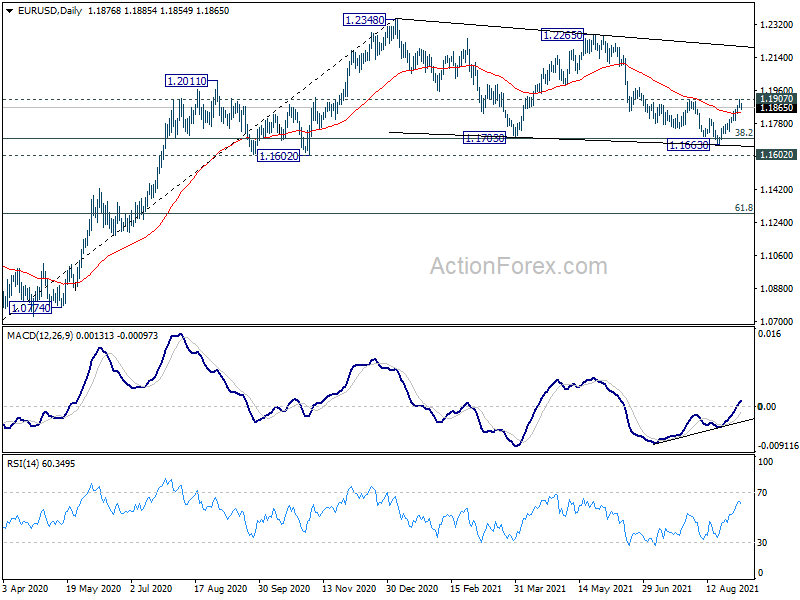

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1860; (P) 1.1884; (R1) 1.1903; More…

Intraday bias in EUR/USD is turned neutral as it retreated after failing to sustain above 1.1907 resistance. Further rise will remain mildly in favor as long as 1.1792 support holds. Sustained break of 1.1907 will indicate that fall from 1.2265, as well as the consolidation pattern from 1.2348, have completed. Near term outlook will be turned bullish for 1.2265/2348 resistance zone. However, on the downside, rejection by 1.1907 followed by break of 1.1792 support will dampen the bullish case, and turn bias back to the downside for 1.1663 support instead.

In the bigger picture, rise from 1.0635 is seen as the third leg of the pattern from 1.0339 (2017 low). Further rally remains in favors long as 1.1602 support holds, to cluster resistance at 1.2555 next, (38.2% retracement of 1.6039 to 1.0339 at 1.2516). However sustained break of 1.1602 will argue that the rise from 1.0635 is over, and turn medium term outlook bearish again. Deeper fall would be seen to 61.8% retracement of 1.0635 to 1.2348 at 1.1289 and below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 1:00 | AUD | TD Securities Inflation M/M Aug | 0.00% | 0.40% | ||

| 1:00 | AUD | TD Securities Inflation Y/Y Aug | 2.50% | 2.60% | ||

| 6:00 | EUR | Germany Factory Orders M/M Jul | 3.40% | -1.00% | 4.10% | 4.60% |

| 8:30 | EUR | Eurozone Sentix Investor Confidence Sep | 19.6 | 19.7 | 22.2 | |

| 8:30 | GBP | Construction PMI Aug | 55.2 | 56.9 | 58.7 |