Products You May Like

Dollar remains overwhelmingly the strongest one for the week, as boosted by intensified Fed hike expectations. Sterling is trying to catch and trading as the next stronger, with special help from buying against Euro. Australian and New Zealand Dollar are taking turns to be the worst performer. Euro and Swiss Franc are not too far away. Canadian Dollar is just mixed, as support by oil prices.

Technically, Yen is displaying some weakness with USD/JPY breaking through 115.05 resistance firmly yesterday. But rally in USD/JPY might not translate into rebound in other Yen crosses. Selling in Yen crosses could come back any time, in particular if risk sentiment turns sour again. The levels to watch include 129.76 in EUR/JPY, 155.38 in GBP/JPY, and 82.13 in AUD/JPY. As long as these levels hold, more downside is still in favor in Yen crosses in general, except USD/JPY.

In Asia, at the time of writing, Nikkei is up 2.18%. Hong Kong HSI is down -0.84%. China Shanghai SSE is up 0.05%. Singapore Strait Times is up 0.25%. Japan 10-year JGB yield is up 0.0100 at 0.169. Overnight, DOW dropped -0.02%. S&P 500 dropped -0.54%. NASDAQ dropped -1.40%. 10-year yield dropped -0.041 to 1.807.

IMF: BoJ’s commitment to prolonged monetary accommodation appropriate

IMF said in a report that BoJ’s commitment to maintaining prolonged monetary accommodation remains “appropriate”. It expects that a “prolonged period of monetary policy accommodation, flexible fiscal policy, and inclusive growth-oriented reforms will be required to durably lift inflation expectations and inflation to the target.”

Further measures could be considered for making monetary support “more sustainable”. On option could be to “steepen the yield curve by shifting the yield target from the 10-year to a shorter maturity”. This could help “mitigate the impact of prolonged monetary accommodation on financial institutions’ profitability”. If underlying inflation momentum remains weak, “cutting the policy rate should be the first option”.

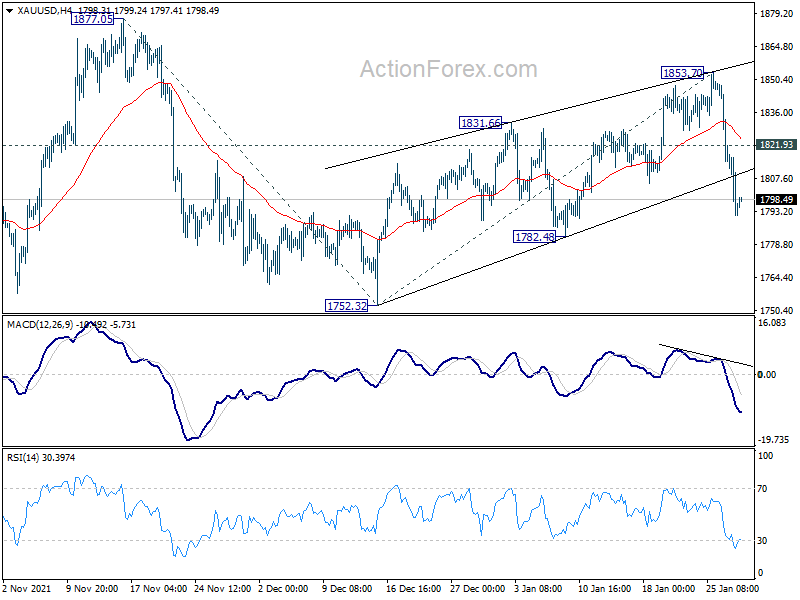

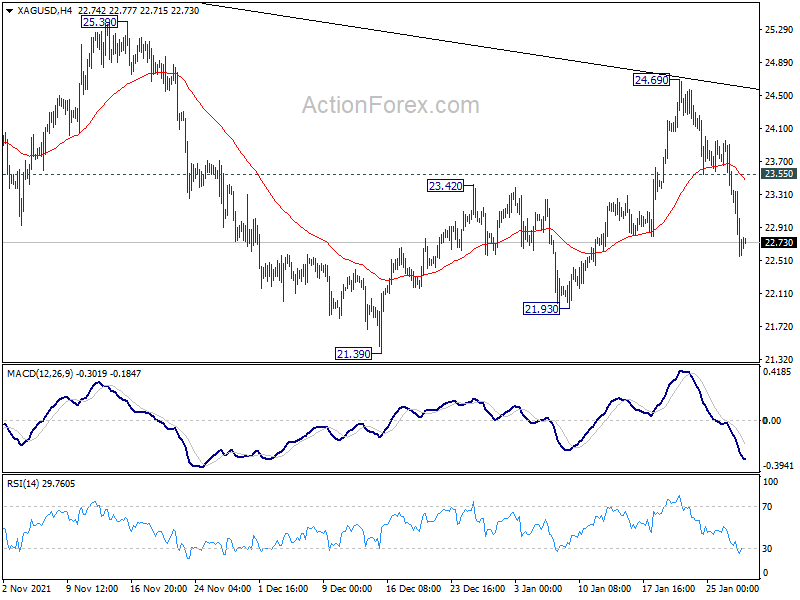

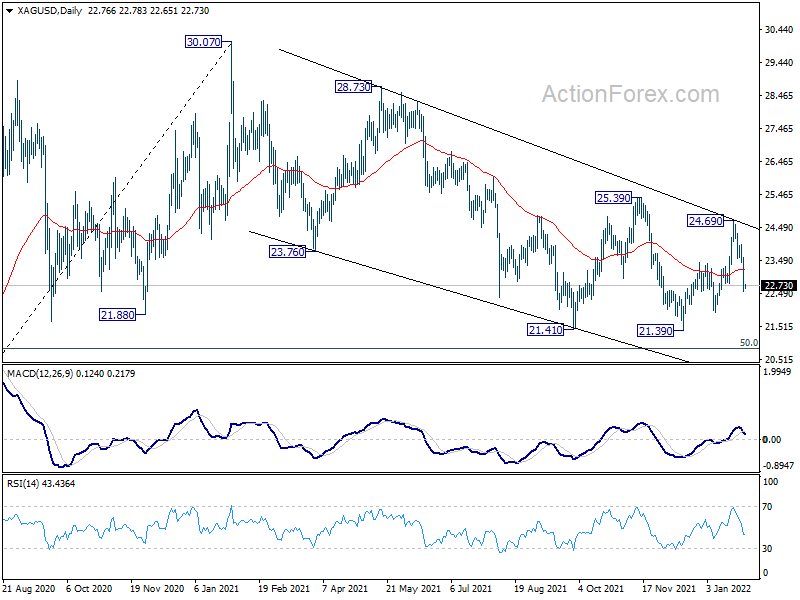

Gold breaks 1800, more downside ahead with Silver

Gold is now back below 1800 handle as fall from 1853.70 extends. The development further affirms the case that rebound from 1752.32 has completed with three waves up to 1853.70. Deeper decline is expected as long as 1821.93 minor resistance holds. Current fall from 1853.70 is see as part of the pattern from 1877.05, which is a down leg inside the medium term range pattern from 1676.65. Break of 1782.48 support will add further credence to this case, and would set the stage for deeper decline through 1752.32 low to 100% projection of 1877.05 to 1752.32 from 1853.70 at 1728.97 eventually.

Silver’s development is also inline with gold. Rebound from 21.39 should have completed with three waves up to 84.69. Deeper decline is expected as long as 23.55 minor resistance holds, to 21.93 support first. Such fall from 24.69 is seen as a leg inside the medium term falling wedge pattern from 30.07. Break of 24.69 would send silver through 21.39 low, to 50% retracement of 11.67 to 30.7 at 20.87 next.

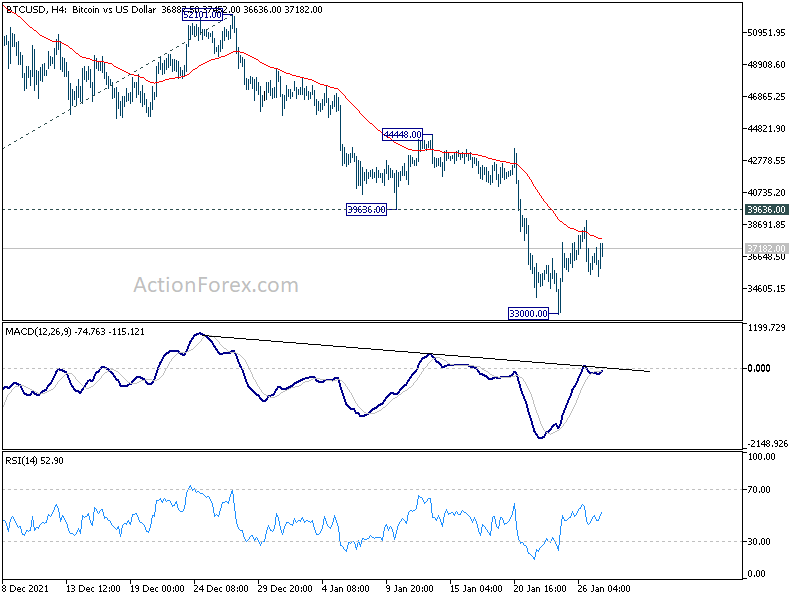

Bitcoin trading sideway, risk still on the downside

Bitcoin stabilized after hitting 33000 and turned sideway. But risk is still staying heavily on the downside with 39636 support turned resistance intact. Current down trend from 68986 could extend with another falling leg, towards 29261 support, which is close to 30k psychological level too. We’d look for bottoming signal around there.

Meanwhile, on the upside, firm break of 39639 will argue that bitcoin has bottomed earlier than expected and bring rebound back towards 55 day EMA (now at 44839). Failure to defend 30k handle will indicate that the larger down trend is still in force for 100% projection of 68986 to 41908 from 52101 at 25023.

On the data front

Japan Tokyo CPI core slowed to 0.2% yoy in January, below expectation of 0.3% yoy. Australia PPI rose 1.3% qoq, 3.7% yoy in Q4, above expectation of 0.9% qoq, 2.7% yoy.

GDP from France and Germany will be the main focuses in European session. France will release consumer spending too while Germany will release import price index. Swiss will release KOF economic barometer while Eurozone will release economic sentiment indicator and M3 money supply.

Later in the day, US personal income and spending, with PCE inflation will be the main focus.

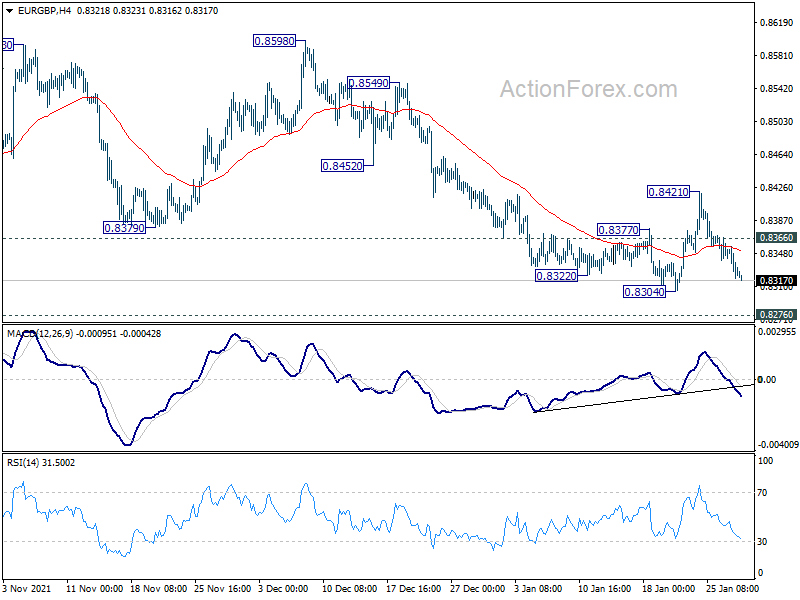

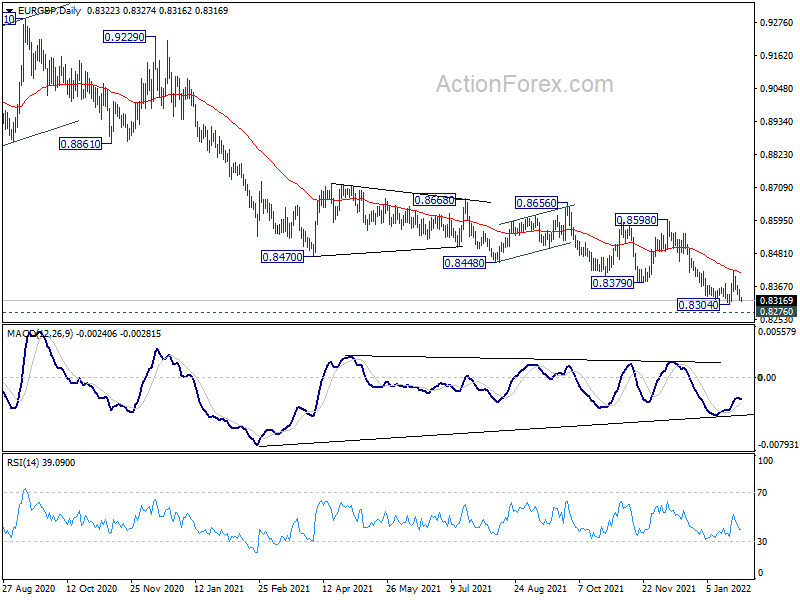

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8313; (P) 0.8336; (R1) 0.8350; More…

Intraday bias in EUR/GBP remains on the downside for 0.8304 support first. Break there will remain larger down trend and target 0.8276 long term support next. On the upside, above 0.8366 minor resistance will turn bias back to the upside for 0.8421 resistance first. Break of 0.8421 will resume the rebound towards 0.8598 key structural resistance.

In the bigger picture, price actions from 0.9499 (2020 high) are still seen as developing into a corrective pattern. Deeper fall could be seen as long as 0.8598 resistance holds, towards long term support at 0.8276. We’d look for bottoming signal around there to bring reversal. Meanwhile, firm break of 0.8598 will now be an early sign of medium term bottoming and bring stronger rebound. However, sustained break of 0.8276 will argue that the long term trend has reversed.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Core Y/Y Jan | 0.20% | 0.30% | 0.50% | |

| 00:30 | AUD | PPI Q/Q Q4 | 1.30% | 0.90% | 1.10% | |

| 00:30 | AUD | PPI Y/Y Q4 | 3.70% | 2.70% | 2.90% | |

| 06:30 | EUR | France Consumer Spending M/M Dec | 0.20% | 0.80% | ||

| 06:30 | EUR | France GDP Q/Q Q4 P | 0.50% | 3.00% | ||

| 07:00 | EUR | Germany Import Price Index M/M Dec | 1.80% | 3.00% | ||

| 08:00 | CHF | KOF Economic Barometer Jan | 106 | 107 | ||

| 09:00 | EUR | Germany GDP Q/Q Q4 P | -0.20% | 1.70% | ||

| 09:00 | EUR | Eurozone M3 Money Supply Y/Y Dec | 6.90% | 7.30% | ||

| 10:00 | EUR | Eurozone Economic Sentiment Indicator Jan | 114.5 | 115.3 | ||

| 10:00 | EUR | Eurozone Services Sentiment Jan | 14.9 | 11.2 | ||

| 10:00 | EUR | Eurozone Industrial Confidence Jan | 15 | 14.9 | ||

| 10:00 | EUR | Eurozone Consumer Confidence Jan F | -8.5 | |||

| 13:30 | USD | Personal Income M/M Dec | 0.50% | 0.40% | ||

| 13:30 | USD | Personal Spending Dec | -0.60% | 0.60% | ||

| 13:30 | USD | PCE Price Index M/M Dec | 0.50% | 0.60% | ||

| 13:30 | USD | PCE Price Index Y/Y Dec | 6.10% | 5.70% | ||

| 13:30 | USD | Core PCE Price Index M/M Dec | 0.50% | 0.50% | ||

| 13:30 | USD | Core PCE Price Index Y/Y Dec | 4.80% | 4.70% | ||

| 13:30 | USD | Employment Cost Index Q4 | 1.20% | 1.30% | ||

| 15:00 | USD | Michigan Consumer Sentiment Index Jan F | 68.6 | 68.8 |