Products You May Like

Euro rebounds strongly today as some ECB policymakers continued to talk up the chance of a July rate hike. Canadian Dollar is following as second strongest, continuing to be supported by strong inflation data. Dollar is not performing too badly for now, as third strongest. On the other hand, New Zealand Dollar remains under pressured after CPI missed expectation. Yen is staying in consolidations in general despite decline attempt against some rivals. Sterling and Swiss Franc are mixed, with Aussie.

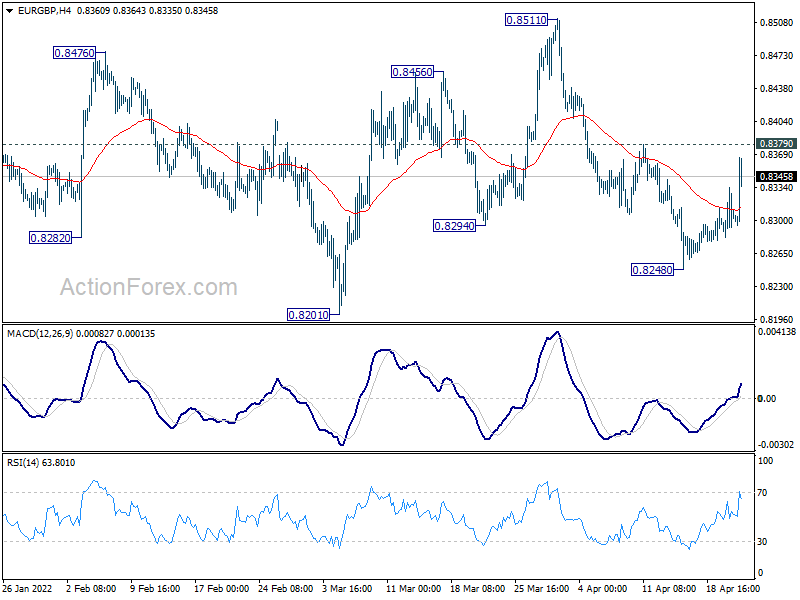

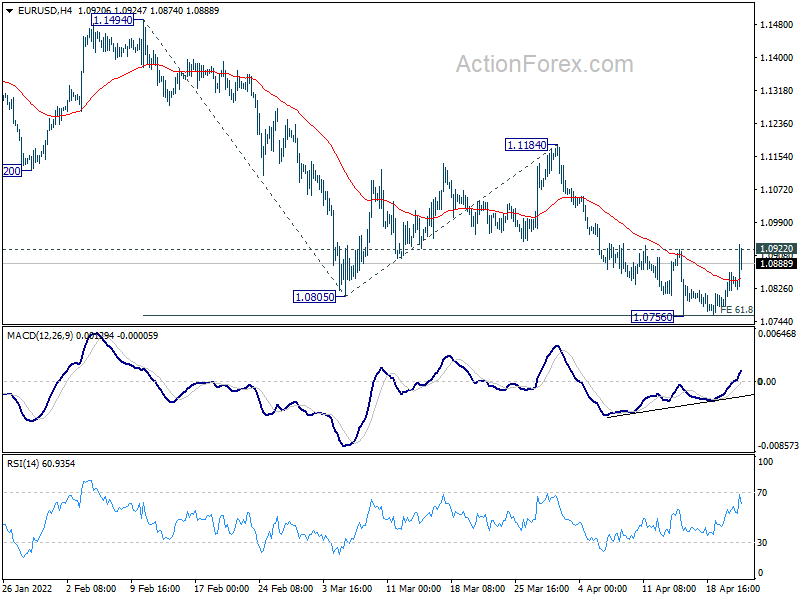

Technically, EUR/USD breached 1.0922 minor resistance but lacks follow through buying. Firm break of this level should confirm short term bottoming and bring stronger rebound back towards 1.1184 resistance. Similarly, firm break of 0.8379 minor resistance in EUR/GBP would bring further rebound back to 0.8511 structural resistance. Developments in these two pairs will be watched to gauge the underlying strength in Euro.

In Europe, at the time of writing, FTSE is up 0.32%. DAX is up 1.41%. CAC is up 1.88%. Germany 10-year yield is up 0.0197 at 0.875. Earlier in Asia, Nikkei rose 1.23%. Hong Kong HSI dropped -1.25%. China Shanghai SSE dropped -2.26%. Singapore Strait times rose 0.39%. Japan 10-year JGB yield dropped -0.0004 to 0.255.

US initial jobless claims dropped to 184k

US initial jobless claims dropped -2k to 184k in the week ending April 16, above expectation of 177k. Four-week moving average of initial claims rose 4.5k to 177k.

Continuing claims dropped -58k to 1417k in the week ending April 9, lowest since February 21, 1970. Four-week moving average of continuing claims dropped -31k to 1482k, lowest since March 21, 1970.

Also released, Philly Fed manufacturing survey dropped from 27.4 to 20.9 in April, below expectation of 20.9.

ECB Lagarde reiterates optionality, gradualism and flexibility in monetary policy

ECB President Christine Lagarde said in a speech, the impact of the factors driving up inflation currently “should fade over time”. But for the near term, “inflationary risks are tilted to the upside”. Over the medium-term, ” risks to the inflation outlook could arise if wages rise by more than anticipated, longer-term inflation expectations move above target or supply conditions durably worsen”.

But so far, “wage growth has remained muted – despite a strong labour market – and inflation expectations in the euro area stand around our target”.

On monetary policy, Lagarde said it will “depend on the incoming data and our evolving assessment of the outlook”. ECB would maintain “optionality, gradualism and flexibility” in the conduct of monetary policy.

ECB de Guindos: July is possible for first hike

ECB Vice President Luis de Guindos said in an interview, the consequences of invasion of Ukraine are “quite clear”, as higher inflation and lower growth. That should be reflected in in June outlook.

He sees “no reason why we should not discontinue our APP programme in July”. But the timing for the first rate hike will depend on the economic projections. “Nothing has been decided so far,” he said.

“From today’s perspective, July is possible and September, or later, is also possible. We will look at the data and only then decide,” he added. Then, the rate hike cycle will “depend on the data” and the “evolution of inflation.

ECB Wunsch: July rate hike is a scenario to consider

ECB Governing Council member Pierre Wunsch said, “without any really bad news coming from that front, hiking by the end of this year to zero or slightly positive territory for me would be a no brainer.”

Also, Wunsch doesn’t rule out ending the asset purchases in June, and raise interest rate in July. “It’s going to of course depend on data,” he said. “If we have another inflation surprise, it’s certainly a scenario that I would consider.”

“There are of course situations where if the shock is very big on the real economy, we would feel more comfortable looking through the inflation development,” he said. But “we’re still in a situation where we’re supportive in terms of monetary policy. Real rates are today very, very negative. So the beginning of the normalization process should be relatively independent of the real economy.”

“We’re still talking about normalization, but I wouldn’t exclude that at some point, if we have second-round effects, wages going up, that monetary policy would have to become restrictive,” he said. “What’s priced in by the markets today to me is on the low side of what might be required to get inflation under control.”

Eurozone CPI finalized at 7.4% yoy in Mar, EU at 7.8% yoy

Eurozone CPI was finalized at 7.4% yoy in March, up from February’s 5.9% yoy. The highest contribution to the annual euro area inflation rate came from energy (+4.36%), followed by services (+1.12%), food, alcohol & tobacco (+1.07%) and non-energy industrial goods (+0.90%).

EU CPI was finalized at 7.8% yoy, up from February’s 6.2% yoy. The lowest annual rates were registered in Malta (4.5%), France (5.1%) and Portugal (5.5%). The highest annual rates were recorded in Lithuania (15.6%), Estonia (14.8%) and Czechia (11.9%). Compared with February, annual inflation fell in two Member States and rose in twenty-five.

NZ CPI rose to 6.9% yoy in Q1, highest since 1990

New Zealand CPI rose 1.8% qoq in Q1, below expectation of 2.0% qoq. For the 12-month period, CPI accelerated from 5.9% yoy to 6.9% yoy, below expectation of 7.1% yoy. That’s nonetheless still the highest annual rate since June 1990 quarter.

StatsNZ said: “The main driver for the 6.9 percent annual inflation to the March 2022 quarter was the housing and household utilities group, influenced by rising prices for construction and rentals for housing.”

“Construction firms have been experiencing many supply-chain issues, higher labour costs, and also higher demand, which have pushed up the cost of building a new house,” senior prices manager Aaron Beck said.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0804; (P) 1.0835 (R1) 1.0887; More…

EUR/USD breached 1.0922 earlier today but quickly retreated. Intraday bias remains neutral for the moment. On the upside, firm break of 1.0922 should confirm short term bottoming at 1.0756. Intraday bias will be back on the upside for 1.1184 structural resistance next. On the downside, though, break of 1.0756 will resume larger down trend.

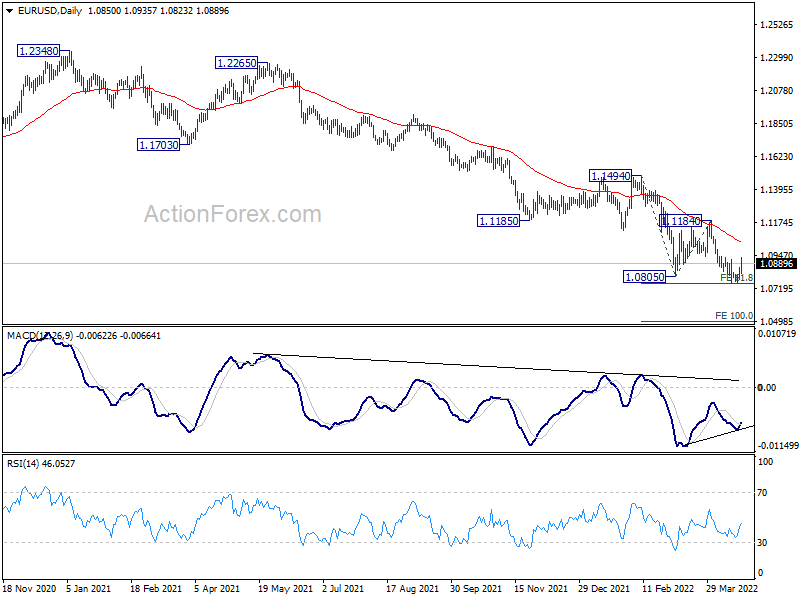

In the bigger picture, the decline from 1.2348 (2021 high) is expected to continue as long as 1.1494 resistance holds. Firm break of 1.0635 (2020 low) will raise the chance of long term down trend resumption and target a retest on 1.0339 (2017 low) next. Nevertheless, break of 1.1494 will maintain medium term neutral outlook, and extending term range trading first.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | CPI Q/Q Q1 | 1.80% | 2.00% | 1.40% | |

| 22:45 | NZD | CPI Y/Y Q1 | 6.90% | 7.10% | 5.90% | |

| 09:00 | EUR | Eurozone CPI Y/Y Mar F | 7.40% | 7.50% | 7.50% | |

| 09:00 | EUR | Eurozone CPI Core Y/Y Mar F | 2.90% | 3.00% | 3.00% | |

| 12:30 | USD | Initial Jobless Claims (Apr 15) | 184K | 177K | 185K | 186K |

| 12:30 | USD | Philadelphia Fed Manufacturing Survey Apr | 17.6 | 20.9 | 27.4 | |

| 14:00 | EUR | Eurozone Consumer Confidence Apr P | -20 | -19 | ||

| 14:30 | USD | Natural Gas Storage | 40B | 15B |