Products You May Like

Overall market sentiment is mixed in Asian session today, with recover seen in Nikkei but selloff in Hong Kong and China. Aussie is extending near term rebound, following Labor’s win in the federal elections over the weekend. Kiwi is also firmer ahead of RBNZ rate hike. On the other hand, Dollar and Canadian are the softer ones. European majors and Yen are mixed for now.

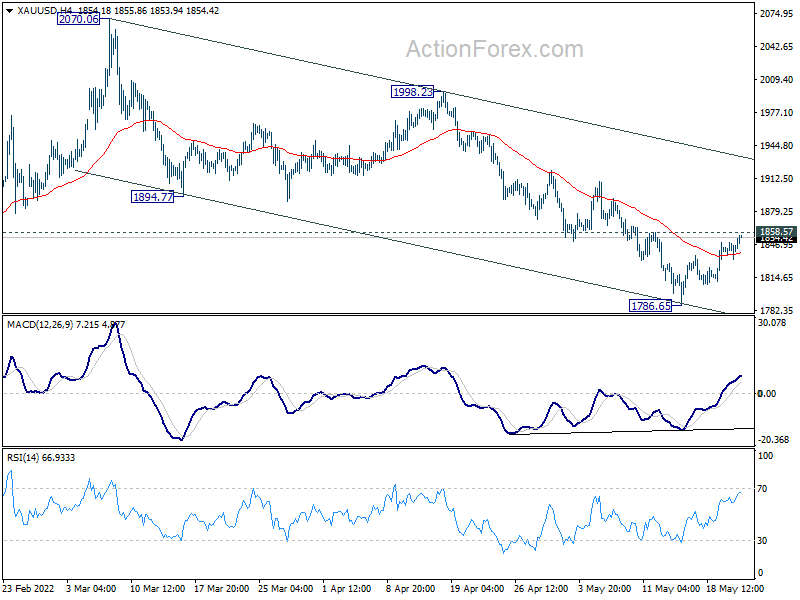

Technically, as Gold’s recovery extends too, attention is on 1858.57 minor resistance. Firm break there will confirm short term bottoming at 1786.65. Stronger rebound would be seen back to channel resistance at around 19333. Such development could be accompanied by deeper pull back in Dollar, in particular against commodity currencies.

In Asia, at the time of writing, Nikkei is up 0.56%. Hong Kong HSI is down -1.95%. China Shanghai SSE is down -0.51%. Singapore Strait Times is down -0.47%. Japan 10-year JGB yield is down -0.0049 at 0.235.

ECB Lagarde: Rate hike could be a few weeks after stopping net asset purchases

ECB President Christine Lagarde told Dutch television over the weekend, “we are going to follow the path of stopping net asset purchase. Then, sometime after that — which could be a few weeks — hike interest rates.” That’s seen as an indication that a rate hike could happen in July, after stopping asset purchases in June.

Governing Council member Klass Knot floated the idea of a 50bps hike earlier. But Lagarde said, “it’s not something that I can tell you at this point in time.” She emphasized, “we need to make sure that this is going gradually enough so that we don’t put the break on this car that is moving. We have to lift the accelerator for sure to slow inflation but we cannot be breaking any speed.”

RBA Kent: Gradual QT also plays a role in stimulus removal

RBA Assistant Governor Christopher Kent said in a speech that while most observers focuses were on the central bank’s 25bps rate hike this month, it also decided to proceed with “quantitative tightening”.

“As the Bank now takes steps to remove the considerable monetary stimulus, increases in the cash rate are the tried and tested measure that will do most of the work…,” he said. “the gradual process of QT will also play a role in this task, but a predictable and modest one.”

“Because the Bank’s bond portfolio will mature gradually, the Bank’s balance sheet and commercial banks’ ES balances will remain large for some years. This means that the cash rate will continue to trade slightly below the cash rate target, but above the rate paid on ES balances. Most importantly though, the Bank will continue to be able to maintain effective control over the cash rate as it withdraws monetary policy stimulus in the period ahead.”

RBNZ rate hike and FOMC minutes

RBNZ is widely expected to continue with its tightening cycle this week, and raise OCR by another 50bps to 2.00%. There is no change in the view that OCR could peak at around 3.4%, as RBNZ projected. But it would now take shorter than earlier expected time to reach the peak of the cycle. RBNZ should reinforce this message to the markets.

From recent comments, Fed official displayed a consensus on the plan of 50bps hike per meeting, at least for the next few ones. FOMC minutes should reflect the discussions and affirm this message too. Meanwhile What next beyond, say July or August, as well as the end point for the year would remain data dependent.

On the data front, PMIs will be the major focuses this week. In addition, Germany Ifo and Gfk sentiment; US durable goods orders, personal income and spending; New Zealand and Australia retail sales, Canada retail sales will also be watched.

Here are some highlights for the week:

- Monday: Germany Ifo business climate.

- Tuesday: New Zealand retail sales; Australia PMIs; Japan PMI manufacturing; UK public sector net borrowing, PMIs; Eurozone PMIs; US PMIs, new home sales.

- Wednesday: RBNZ rate decision; Germany GDP final, Gfk consumer climate; Swiss Credit Suisse economic expectations; US durable goods orders, FOMC minutes.

- Thursday: Japan corporate services prices; Australia private capital expenditure; Canada retail sales; US GDP revision, jobless claims, pending home sales.

- Friday: Japan Tokyo CPI; Australia retail sales; Eurozone M3 money supply; US goods trade balance, personal income and spending and PCE inflation.

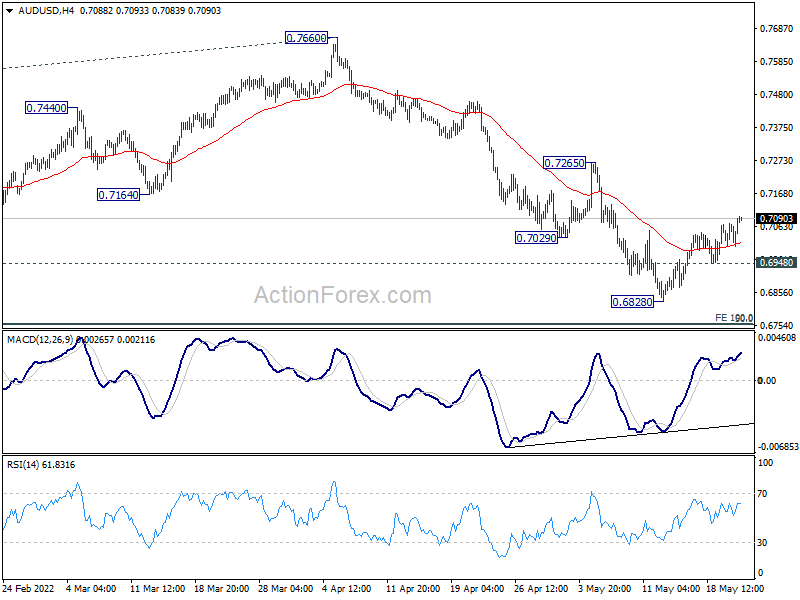

AUD/USD Daily Report

Daily Pivots: (S1) 0.7004; (P) 0.7039; (R1) 0.7075; More…

Intraday bias in AUD/USD remains on the upside at this point. Rebound from 0.6828 short term bottom is on track to 55 day EMA (now at 0.7183). Break there will target 0.7265 resistance next. On the downside, though, break of 0.6948 will resume larger fall from 0.8006 through 0.6828 low, and target 0.6756/60 medium term fibonacci level next.

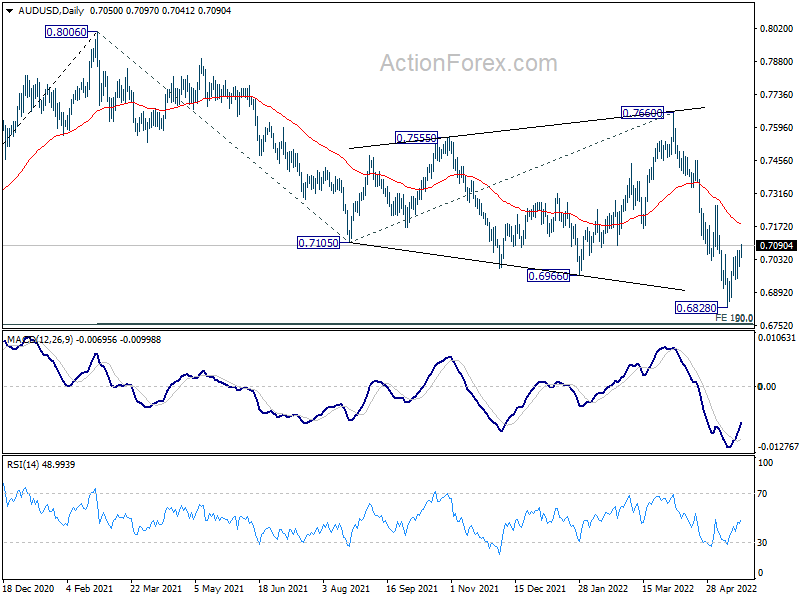

In the bigger picture, price actions from 0.8006 are seen as a corrective pattern to rise from 0.5506 (2020 low). Deeper fall could be seen to 50% retracement of 0.5506 to 0.8006 at 0.6756. This coincides with 100% projection of 0.8006 to 0.7105 from 0.7660 at 0.6760. Strong support is expected from 0.6756/60 cluster to contain downside to complete the correction. However, sustained break of 0.6756/60 would argue that AUD/USD is indeed already in a medium term down trend.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | Rightmove House Price Index M/M May | 2.10% | 1.60% | ||

| 08:00 | EUR | Germany IFO Business Climate May | 91.4 | 91.8 | ||

| 08:00 | EUR | Germany IFO Current Assessment May | 97.2 | 97.2 | ||

| 08:00 | EUR | Germany IFO Expectations May | 85.8 | 86.7 |