Products You May Like

Sterling is trading as the strongest one for today so far, even though there is not clear follow through buying except versus Yen. The Pound is supported by UK Finance Minister Jeremy Hunt’s decision that the government will reverse “almost all” the tax measures in the Growth Plan announced just three weeks ago. Yen’s decline continues but selloff is mainly seen against European majors. Dollar is trading on the soft side, and would remain so if US stocks could extend the pre-session rebound.

Technically, both EUR/JPY and GBP/JPY are edging closer to near term resistance at 145.62 and 169.10 respectively. Decisive break of these levels will confirm larger up trend resumption. Given that USD/JPY bulls are on the guard of Japan’s intervention at around 150 handle, rally in EUR/JPY and GBP/JPY could help push EUR/USD and GBP/USD higher. But, the prerequisite is there is no clear deterioration in sentiment in stock and bond markets.

In Europe, at the time of writing, FTSE is up 0.83%. DAX is up 1.42%. CAC is u 1.21%. Germany 10-year yield is down -0.123 at 2.230. Earlier in Asia, Nikkei dropped -1.16%. Hong Kong HSI rose 0.15%. China Shanghai SSE rose 0.42%. Singapore Strait Times dropped -0.78%. Japan 10-year JGB yield dropped -0.0012 to 0.253.

US Empire State manufacturing dropped to -9.1 in Oct

US Empire State Manufacturing index dropped sharply from 1.5 to -9.1 in October. 23% of respondents reported that conditions had improved while 32% said worsened. After falling significantly over the prior three months, the prices paid index rose nine points to 48.6. The prices received index held steady at 22.9.

Index for future conditions dropped from 8.2 to -1.8. indicating that firms do not expect conditions to improve over the next six months.

Japan Suzuki: Will take decisive action on excessive volatility

There is no clear sign of intervention by Japan so far, as USD/JPY is trading in tight range close to 32-yr high. Finance Minister Shunichi Suzuki just said, “if we see excessive volatility caused by speculative moves, we will take decisive action. There is no change in this view at all.”

Separately, BoJ Governor Haruhiko Kuroda said in a parliamentary session, Japan’s economy is in the midst of recovery from COVID-19. Higher commodity prices, on the back of the situation in Ukraine, have been leading to an outflow of income from Japan to overseas, adding downward pressure on the economy.”

“For now, we think it appropriate to continue with monetary easing because it’s necessary to support the economy and achieve our inflation target in a sustainable and stable fashion accompanied by wage growth,” he added.

NZ BNZ services dropped to 55.8 in Sep

New Zealand BusinessNZ Performance of Services Index dropped from 58.6 to 55.8 in September. Looking at some details, activity/sales dropped from 67.5 to 59.2. Employment ticked down from 50.7 to 50.5. New orders/business dropped from 66.6 to 62.9. Stocks/inventories dropped from 59.6 to 54.9. Supplier deliveries was unchanged at 49.7.

BNZ Senior Economist Craig Ebert said that “the composite PCI held together at 54.4 in free-weighted terms, while the GDP weighted composite came in at 55.4, from 58.2 in August. These marry with our view that Q3 GDP increased about 1.0%”.

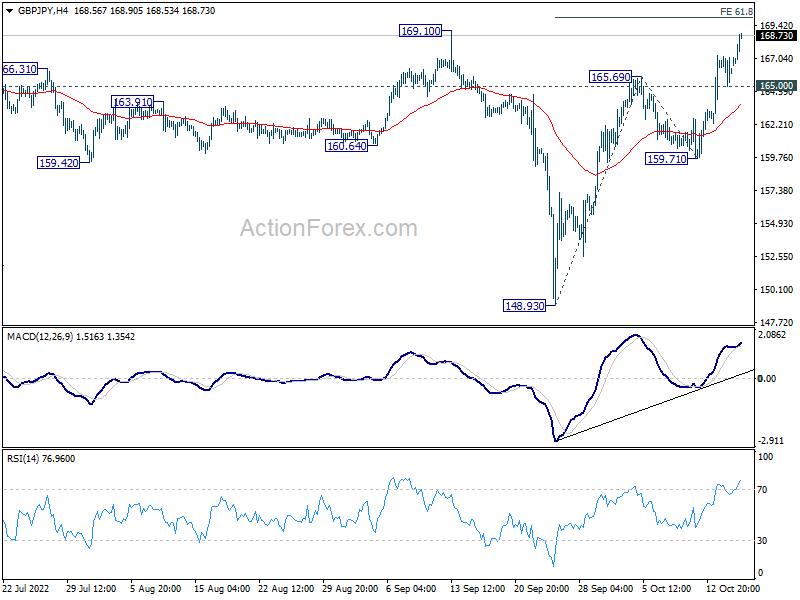

GBP/JPY Mid-Day Outlook

Daily Pivots: (S1) 165.15; (P) 166.18; (R1) 167.34; More…

GBP?JPY’s rally continues today and intraday bias stays on the upside for 169.10. Firm break there will target 61.8% projection of 148.93 to 165.69 from 159.71 at 170.06, and then 100% projection at 176.47. On the downside, below 165.00 minor support will turn Intraday bias neutral first.

In the bigger picture, current development suggests that up trend from 123.94 (2020 low) is still in progress. Sustained break of 61.8% retracement of 195.86 (2015 high) to 122.75 (2016 low) at 167.93 will pave the way to retest 195.86 high. This will now remain the favored case as long as 148.93 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | Business NZ PSI Sep | 55.8 | 58.6 | ||

| 23:01 | GBP | Rightmove House Price Index M/M Oct | 9 | 0.70% | ||

| 04:30 | JPY | Tertiary Industry Index M/M Aug | 0.70% | 0.40% | -0.60% | |

| 04:30 | JPY | Industrial Production M/M Aug F | 3.40% | 2.70% | 2.70% | |

| 12:30 | USD | Empire State Manufacturing Index Oct | -9.1 | -1 | -1.5 | |

| 14:30 | CAD | BoC Business Outlook Survey |