Products You May Like

Euro’s broad based selloff continues today, even though it’s still holding in range against Dollar and Sterling. But overall, European majors are weak. The greenback is somewhat capped by falling benchmark treasury yield. Yen is firm on risk-off sentiment but it’s slightly out-performed by Aussie. In other markets, stocks are generally pressured in Europe while US futures are down. Gold is back above 1900 handle but lacks follow through buy yet. WTI crude oil resumes recent rally with new wave of buying.

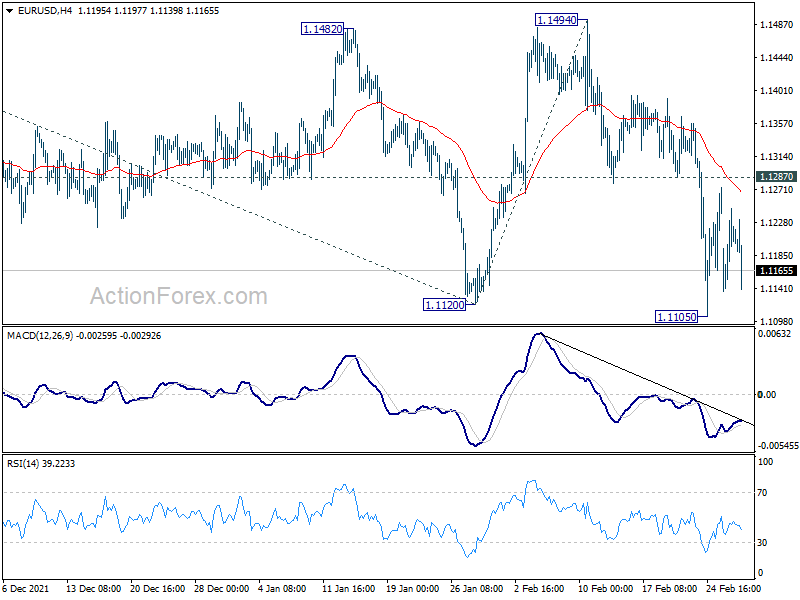

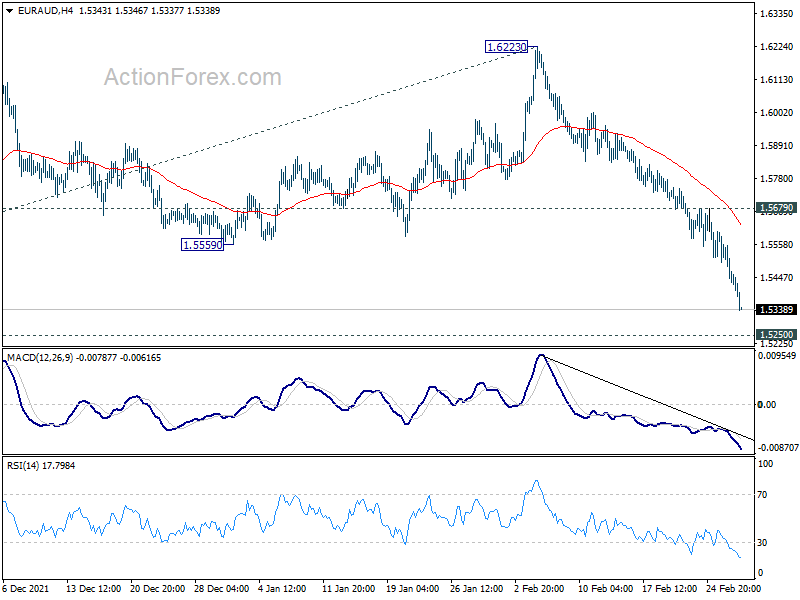

Technically, Euro’s weakness will remain a focus. EUR/CHF’s decline extends below 1.0277 temporary low. EUR/AUD’s break of 1.5354 support suggests that larger down trend is ready to resume through 1.5250 low. A question is when EUR/USD will join the party and break through 1.1105 temporary low.

In Europe, at the time of writing, FTSE is down -0.78%. DAX is down -2.26%. CAC is down -2.32%. Germany 10-year yield is down -0.095 at 0.038. Earlier in Asia, Nikkei rose 1.20%. Hong Kong HSI rose 0.77%. China Shanghai SSE rose 0.77%. Singapore Strait Times rose 1.12%. Japan 10-year JGB yield dropped -0.0040 to 0.181.

Canada GDP flat in Dec, grew 0.2% in Jan

Canada GDP was flat in December, matched expectation of 0.0% mom. The 0.1% mom growth in services-producing industry was offset by the -0.1% mom decline in goods-producing industries. 14 of 20 industrial sectors grew.

Advance information indicates a 0.2% mom growth in real GDP in January, led by retail, construction, finance and insurance as well as the professional, scientific and technical services sector.

UK PMI manufacturing finalized at 58 in Feb, production and new orders both accelerate

UK PMI Manufacturing was finalized at three-month high of 58.0 in February, up from 57.3 in January. Markit said output and new orders expanded at quicker rates. New export orders decreased. Input price inflation remained elevated.

Rob Dobson, Director at IHS Markit, said: “February saw rates of expansion in UK manufacturing production and new orders both accelerate. Growth was boosted by stronger domestic demand and by firms catching up on delayed work as material shortages and supply chain disruptions started to dissipate…. However, the trend in new export orders is less positive, slipping back into contraction after January’s short-lived uptick….

“Inflationary pressure also remained elevated across the manufacturing sector… That said, rates of inflation for input costs and output charges eased further. Although this easing may have provided some temporary respite, signs that energy and oil prices may stay high is a further cause for concern.”

Eurozone PMI manufacturing finalized at 58.2 in Feb, a largely positive month

Eurozone PMI Manufacturing was finalized at 58.2 in February, down slightly from January’s 58.7. Markit said demand for Eurozone goods rose at fastest rate since last August. Supplier delivery times lengthened to weakest extent for over a year, but inflation remained steep.

Looking at some member states, the Netherlands rose to 3-month high at 60.6. Germany dropped to 58.4 while Austria dropped to 58.4. Italy was unchanged at 58.3. Ireland dropped to 11-month low at 57.8. Greece dropped to 7-month low at 57.8. France rose to 6-month high at 57.2. Spain rose to 3-month high at 56.9.

Joe Hayes, Senior Economist at IHS Markit said: “Don’t let the drop in the headline PMI distract from what should be viewed as a largely positive month for the euro area manufacturing sector in February. Demand for goods is trending higher, with the rate of expansion accelerating to a six-month high. Underlying sales conditions are clearly strengthening as Europe overcomes the Omicron wave of COVID-19 and businesses step up their recovery efforts.”

Germany PMI Manufacturing was finalized at 58.4 in February, down from January’s 59.8. Markit said there were sharp rise in backlogs as growth in the new orders outstripped output. Factory cost inflation slipped further from recent highs. Incidence of supply delays was lowest since November 2020.

France PMI Manufacturing was finalized at six-month high of 57.2 in February, up from January’s 55.5. Markit said manufacturing output increased at fastest rate since last July. Demand for goods improved despite steep output price inflation. Capacity pressures intensified as supply issues persisted.

RBA stands pat and be patient

RBA left cash rate target unchanged at 0.10% as widely expected. The board maintained that it “will not increase the cash rate until actual inflation is sustainably within the 2 to 3 per cent target range.”. For now, it is “too early to conclude that it is sustainably within the target range”, and RBA is “prepared to be patient”.

Australia AiG manufacturing rose to 53.2, edged back into expansion

Australia AiG Performance of Manufacturing Index rose 4.8 pts to 53.2 in February. Production rose 2.7 to 54.6. Employment dropped -1.9 to 43.5. Average wages rose 1.4 to 64.9. Input prices dropped -6.7 to 75.6. But selling prices rose 1.4 to 64.9.

Innes Willox, Chief Executive of Ai Group said: “Australia’s manufacturing sector edged back into expansion during February following the sharp labour and supply chain disruptions of the December-January period. Price and wage pressures continued in February with some easing in the pace of increase in input prices. At the same time, selling prices accelerated suggesting further recovery of earlier cost increases.”

Japan PMI manufacturing finalized at 52.7, new orders stagnates and input prices rose

Japan PMI Manufacturing was finalized at 52.7 in February, down from January’s 55.4. Markit said there was renewed fall in output amid near-stagnation in new orders. Input prices rose at sharpest pace since August 2008. Stocks of purchases had survey-record increase amid delays and shortages.

Usamah Bhatti, Economist at IHS Markit, said: “February PMI data pointed to a softer expansion in the Japanese manufacturing sector. The rate of growth eased to a five-month low, however, amid a renewed reduction in production levels and a broad stagnation in new orders… input price pressures intensified further, with average cost burdens rising at the sharpest pace in thirteen-and-a-half years… manufacturers commented that the degree of optimism regarding the 12-month outlook for output eased to a six-month low in February… This is broadly in line with the IHS Markit prediction for industrial production to grow 5.9% in 2022.”

China Caixin PMI manufacturing rose to 49.1 in Feb, returned to growth

China Caixin PMI Manufacturing rose from 49.1 to 50.4 in February, above expectation of 49.5. Caixin said output returned to growth amid quickest rate in new work for eight months. Pandemic continued to weigh on export sales. Business confidence picked up to the highest since last June.

Wang Zhe, Senior Economist at Caixin Insight Group said: “Overall, manufacturing activity expanded in February. Supply recovered, while demand more clearly improved. The level of optimism about the future business outlook increased further. However, the job market remained under high pressure. And we still need to keep an eye on inflationary pressure.

EUR/AUD Mid-Day Outlook

Daily Pivots: (S1) 1.5390; (P) 1.5487; (R1) 1.5539; More…

EUR/AUD drops to as low as 1.5336 so far and intraday bias remains on the downside. Break of 1.5354 support should now pave the way to 1.5250 low. Decisive break there will resume larger down trend from 1.9799. Next near term target will be 100% projection of 1.6343 to 1.5354 from 1.6223 at 1.5143. On the upside, break of 1.5679 resistance is needed to indicate short term bottoming. Otherwise, outlook stays bearish in case of recovery.

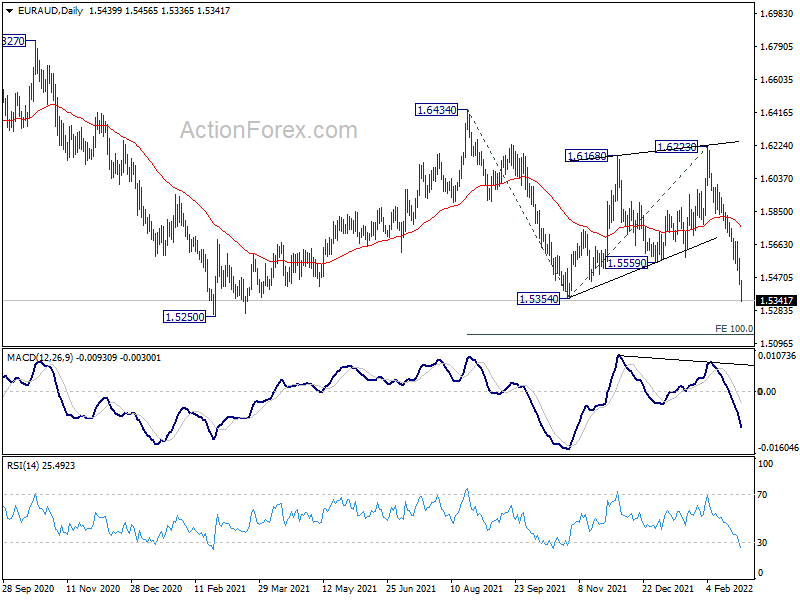

In the bigger picture, price actions from 1.5250 low are seen as a corrective pattern. Further extension could be seen and another rise cannot be ruled out. But strong resistance should be seen at 38.2% retracement of 1.9799 to 1.5250 at 1.6988. Larger down trend from 1.9799 (2020 high) is in favor to extend through 1.5250 at a later stage. Next target is 61.8% retracement of 1.1602 (2012 low) to 1.9799 at 1.4733

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | AUD | AiG Performance of Mfg Index Feb | 53.2 | 48.4 | ||

| 00:30 | AUD | Current Account (AUD) Q4 | 12.7B | 14.3B | 23.9B | 22.0B |

| 00:30 | JPY | Manufacturing PMI Feb F | 52.7 | 52.9 | 52.9 | |

| 01:00 | CNY | Manufacturing PMI Feb | 50.2 | 49.9 | 50.1 | |

| 01:00 | CNY | Non-Manufacturing PMI Feb | 51.6 | 50.9 | 51.1 | |

| 01:45 | CNY | Caixin Manufacturing PMI Feb | 50.4 | 49.5 | 49.1 | |

| 03:30 | AUD | RBA Interest Rate Decision | 0.10% | 0.10% | 0.10% | |

| 08:30 | CHF | SVME PMI Feb | 62.6 | 64.7 | 63.8 | |

| 08:45 | EUR | Italy Manufacturing PMI Feb | 58.3 | 59.2 | 58.3 | |

| 08:50 | EUR | France Manufacturing PMI Feb F | 57.2 | 57.6 | 57.6 | |

| 08:55 | EUR | Germany Manufacturing PMI Feb F | 58.4 | 58.5 | 58.5 | |

| 09:00 | EUR | Eurozone Manufacturing PMI Feb F | 58.2 | 58.4 | 58.4 | |

| 09:30 | GBP | Manufacturing PMI Feb F | 58 | 57.3 | 57.3 | |

| 09:30 | GBP | Mortgage Approvals Jan | 74K | 72K | 71K | |

| 09:30 | GBP | M4 Money Supply M/M Jan | 0.10% | 0.40% | 0.10% | |

| 13:00 | EUR | Germany CPI M/M Feb P | 0.90% | 0.90% | 0.40% | |

| 13:00 | EUR | Germany CPI Y/Y Feb P | 5.10% | 5.10% | 4.90% | |

| 13:30 | CAD | GDP M/M Dec | 0.00% | 0.00% | 0.60% | |

| 14:30 | CAD | Manufacturing PMI Feb | 56.2 | |||

| 14:45 | USD | Manufacturing PMI Feb F | 57.5 | 57.5 | ||

| 15:00 | USD | ISM Manufacturing PMI Feb | 57.9 | 57.6 | ||

| 15:00 | USD | ISM Manufacturing Prices Paid Feb | 77.5 | 76.1 | ||

| 15:00 | USD | ISM Manufacturing Employment Index Feb | 54.5 | |||

| 15:00 | USD | Construction Spending M/M Jan | -0.50% | 0.20% |